|

4 Ways to Pay Off a Car Loan Fast

Looking for ways to pay off your car loan quickly? I’ve been there. Four months into my first full-time job, I made an incredibly stupid decision. I purchased an expensive vehicle. And I took out a loan to do it. A $20,000 loan. It is important to note that the $20,000 figure was a completely arbitrary number I chose, at random, because I thought it sounded like an adult-level dollar amount to pay for a car. I did not adjust this figure based on my annual salary or the amount of money I had tucked away in my savings account. Now, before you think I’m completely financially inept, I will share a few things I did right:

These were good places to start but would have been completely unnecessary, if I had played my cards right. The fact of the matter is that I walked out of that dealership with a pretty car and $20,000 of debt. You can buy a lot of stuff with $20,000. That is a lot of zeros. Don’t get me wrong: I love my vehicle.I drive a lot to visit friends and family, and my car is reliable, comfortable, and has Bluetooth capability, which means I can rock out to the Moana soundtrack as I cruise through the McDonald’s drive-thru. But as wonderful as my car is, that $20,000 price tag was not something I wanted hanging over my head for four years. Instead, I decided to shoot for the impossible: I wanted to own my car (and free myself from that car payment) in half that time. Before anyone sticks their nose in the air and tries to convince themselves that I must be some sort of superpowered, magical wizard to make this fairy tale of paying off my car loan faster come true, I will start by saying that I do not make an exuberant amount of money. I am not bathing in Benjamins. I do not wallpaper my room with the faces of Andrew Jackson and Ulysses S. Grant. I make a modest (yet, totally livable) income of less than $40k a year. I did not have superhuman abilities that somehow made it easier for me to save money and pay off my debt. What I had was a vision, and the discipline to make that vision a reality. Here’s How I Paid Off My Car Loan Fast1. I identified my spending priorities.Once I secured a stable income and the paychecks started coming in, I had to decide what I wanted my dollars to do for me. At the time I took out my car loan, I was still making my final payments on my student loans. I also had to cover essentials like rent, groceries, and gasoline to get me to work. But even with these obligations, I had dollars left over in my account, and it was up to me to decide how I wanted to spend them. Did I want to blow them on Starbucks frappuccinos, new clothes, concert tickets and artisan tacos, drowning myself in luxuries but still stressed about my bills and living paycheck to paycheck? Or did I want to max out my 401k, pad my savings account and make extra payments on my loans? The second option isn’t as glamorous on the surface, but it leads to financial independence—my true goal—whereas the first option leads to an expensive life that requires increasing amounts of effort, stress and income to maintain. Once I established debt repayment and financial independence as my top priorities, I simply had to spend in alignment with those priorities. Which leads us to number two. 2. I started a budget.I procrastinated on this one for a long time, because the thought of making a plan for my money sounded about as fun as a snugglefest with a Yeti. Budgeting was a trial-and-error process for me at first; I started with my own spreadsheet (which quickly failed because it was boring and inflexible) and then I moved to Mint (which is decent as far as free budgeting software goes, but doesn’t allow you to plan ahead for larger, one-time expenses like new tires or Christmas shopping—a serious pitfall). In the end, I settled on a budgeting platform called You Need A Budget (YNAB). Their built-in Loan Planner makes it easier than ever to strategize and visualize the potential for paying off your car loan quickly! Budgeting with YNAB was, and continues to be, one of the best decisions I’ve ever made, both for my finances and my quality of life as a whole. I would recommend it to anybody. Someday in the future, I’ll write an entire post dedicated to how awesome it is, but for now, know this: According to YNAB’s website, new users save $300 on average their first month with the software and $6,000 in the first year. You know how there are mirrors on your vehicle so you can see into your blind spots? That’s what YNAB (and budgeting) does for your finances. It removes your ability to make excuses for your poor spending behavior because the numbers are on the table and they say you went to Chipotle four times last week. (Unfortunately, this is a true story.) WHY are you ordering chips and guac when you own a car you still haven’t paid for? PRI-OR-I-TIES. 3. I funded my priorities and threw out, literally, everything else.Once I solidly rooted myself in my priorities, everything else became a luxury. As I became more financially aware, I realized “harmless” spending was not harmless at all. In actuality, it was something that came directly between me and my relentless quest for financial independence. I will admit that this ruthless prioritization was not always fun. Sometimes it sucked. It sucked to watch my coworkers order mouthwatering craft burgers for lunch while I was eating a less-than-delicious salad I brought from home. It sucked to turn down happy hour because I knew ten-dollar, sugar-dusted martinis wouldn’t fit anywhere into my budget (or my waistline). But my focus was never on these short-term pleasures, and the pain of saying no to them was fleeting. I was playing the long game, and financial independence was more important to me than literally anything else money could buy. So I packed my lunch every day, instead of joining my colleagues for lunch at a trendy downtown restaurant. I rented books from my local library for free, instead of purchasing tickets to the movies. I swapped clothing with my friends in lieu of buying new. And I did this knowing that every dollar I saved brought me one step closer to unshackling myself from the burden of my debt, forever. 4. I aggressively started paying back my debt.Once I had identified my priorities, set my budget, and trimmed the fat from my spending, I started throwing all my spare income toward my car loan and began making additional payments. Earlier this year, I called my financial institution to increase the amount of my monthly loan payments—I had been watching my budget and knew I could fork over some extra money while still having plenty of breathing room. At some point, I realized there was an inverse relationship between my debt and my goal for financial independence; as the principle left on my loan shrank, my desire to pay off my car loan fast. I sold old junk on eBay for some extra cash and saved money on food by batch cooking. I delayed purchases until I truly needed them. I practiced gratitude and was thankful for all that I already owned. And, last week, it finally paid off.I wrote my final check to the bank and paid my car loan off in full. After one year and nine months, this sweet, blue baby ride is completely, totally, 100% mine. Set your sights on your goals, whatever they are, and pursue them relentlessly. Don’t give up. The view is best from the top. Did you enjoy this post? You can read more from Amanda over at burstofintention.com. Newly motivated to start budgeting to pay off your car loan quickly? Try YNAB for free (no credit card needed for sign up) to create your own debt-busting budget. The post 4 Ways to Pay Off a Car Loan Fast appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/11/4-ways-to-pay-off-car-loan-fast.html November 02, 2021 at 06:42AM

0 Comments

5 Ways To Pay Off Your Mortgage Quickly

A lot of people are, understandably, interested in demolishing all of their debt and that includes figuring out how to pay off a mortgage quickly. It’s an admirable goal, and living a debt-free life can open doors to a whole new world of possibilities. Want to travel around the globe? Cool—with some careful planning, a valid passport, and savvy saving, the sky’s the limit! Ready to quit your job to homeschool the kids? You can afford to type up that resignation letter and start surfing Pinterest for curriculum ideas. Dream about filling a bathtub up with quarters and bathing in it like you’re Scrooge McDuck? Well, that’s kind of weird, my friend, but I’m not here to judge you. Eliminating your monthly mortgage payment can significantly increase your cash flow—and just about everyone likes having extra money on hand. So let’s talk about how to pay off a mortgage faster. How to Pay Off a Mortgage QuicklyOkay, let’s do this in five quick tips. Ready? #1 Pay MoreLet’s start with number one, because starting with any other number wouldn’t make much sense: pay more. Yep. Have more money and then budget that money to pay more towards your mortgage. Presto Change-o, no more mortgage. So, yeah, that one’s important. Top notch personal finance advice, truly. And then the next step is…well, wait, it will come to me. Okay, you know what? I forgot the other four. There were going to be five. Number one is to pay more, and that’s a good one. I had a strong start here. Alright, I guess it’s just the one tip, which is a bummer because five tips sounds better, and frankly, number three would have amazed you, but to pay off your home loan quickly, you have to pay more. However, this one tip is such a good tip, I think it’s fair to expand upon it. How to Pay More to Pay Off Your Mortgage#2 Increase Frequency of Mortgage PaymentsIt seems like cheating to start on number two when this is really a new list now, you might be thinking, but what you need to be thinking about is how to pay off your mortgage quickly. Focus, people! A quick and relatively painless way to pay more towards your mortgage payment is to pay bi-weekly instead of monthly. Breaking your payments into two each month, even if you don’t increase the overall amount of your monthly payment, results in one extra payment each year. With 52 weeks in a year, bi-weekly payments means you’ll make 26 total payments, or 13 monthly payments…without impacting your monthly budget much. Check out YNAB’s Loan Planner tool to see how how making extra payments will affect your own outcome! #3 Make Extra Payments Towards Mortgage PrincipalWhen putting extra money towards your mortgage, it’s important to specify to your mortgage company that you want the overage applied to principal. Interest makes up a significant portion of your mortgage, and since it’s calculated on the principal balance, paying down the principal reduces the amount of interest that you’ll pay on a fixed-rate loan. That extra payment you’ll be making in the above bi-weekly scenario? Mark it as going towards your principal for that extra debt paydown oomph.

#4 Refinance to a Shorter Loan TermIf you have a traditional 30-year fixed rate mortgage, refinancing to a 15-year loan means you’d be paying it off in…15 years. (The good advice just doesn’t stop here, folks, and it’s free!) Yes, your monthly payment will be higher and you’re likely to have some closing costs associated with this plan but 15-year mortgages often come with a lower interest rate and you’ll be paying a lot less interest over the life of the loan due to the reduced timeline. Learn more about if you should refinance. #5 Get Clear on PrioritiesWhen YNAB’s founder, Jesse Mecham, was 25 years old, he had a new baby and didn’t own a home yet, so he did what any normal 25-year-old would do (no, not really) and wrote “Pay off mortgage by the time I’m 30” on a notecard and stuck it in his wallet. And then he did it. Do you know how? (Okay, we just went through this whole “you have to pay more” thing and you don’t know how?) Let’s move on to why then: Because he wanted to. He wanted that so much that he stayed focused on it. He lived in a mostly unfurnished home that echoed a lot and his friends and family members thought it was all very odd. He worked harder and he sacrificed other things because he wanted to pay a mortgage off enough to write that down on a notecard and stick it in his wallet before he even had a mortgage. So decide if you want to pay off your mortgage quickly. If that’s not one of your financial goals, that’s okay. A lot of people don’t mind having a mortgage; interest rates are low, real estate is an investment, maybe they have a prepayment penalty, or have student loans that take precedence, but for whatever reason, it’s not high on their priority list. There’s nothing wrong with that. Paying a mortgage off quickly has to be your priority if you want to make it happen. You choose your own intensity; maybe you get a side hustle, perhaps you skip take-out and vacations, but you pay more and you feel good doing it because you’re working towards something you really want. And one day you’re sitting in your bathtub full of quarters in that home that you own free and clear, thinking, “That YNAB writer said this was weird, but so was the way she numbered that list.” I’m looking forward to that day for you, because it will all have worked out well for both of us. Ready to find room in the budget to pay more towards your mortgage? Try YNAB free for 34 days. The post 5 Ways To Pay Off Your Mortgage Quickly appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/11/5-ways-to-pay-off-your-mortgage-quickly.html November 02, 2021 at 06:42AM

Which Comes First: Emergency Fund or Pay Off Debt?

You might be asking yourself, “Should I build my emergency fund or pay off debt first?” If you’re debating between paying off debt or saving more cash, your emergency fund should come first! You heard that right, debt—we’ll deal with you later (soon, but later). See, they’re both good options, but there is a gooder, er, better option. Whenever you’re dealing with multiple financial goals, they all elbow for your attention (and your dollars). But there is a method to this madness, and that’s what I’d like to talk about today. Should I Build My Emergency Fund or Pay Off Debt First?Before we can talk about saving for emergencies or crushing your debt to smithereens, there’s the matter of your basic needs: 1. Cover Your Basic NeedsFirst things first, you have to cover your essentials with the dollars you currently have. These are things that:

Typically, they’re expenses related to survival:

And how far out are they covered? Just next month? If you’re faced with uncertainty around income, you might want to stop at this step and use your cash to cover these essentials a few months out. Once you’ve got those covered, you move on to… 2. Cover Your Non-Monthly (But Necessary) ExpensesThese expenses are the purchases that you know are coming, but they don’t happen every month. These might be things like:

When you’re looking at the total cost of a month of your life, you want to include these one-off expenses. You can think of this as preventing future debt. By breaking these larger costs down into monthly chunks, it’s not a huge blow when the multi-hundred dollar bill comes due. You’ll have the money already set aside and it won’t need to go on the credit card. Why Saving for the Basics Matters So MuchIt’s easy to see why paying our monthly bills is the top priority. You need a roof over your head, and food to keep you alive. But what about those irregular expenses? It’s harder to put aside dollars for car repairs when your car seems totally fine—especially when you’re wrestling with debt! The thing is, if you don’t fund your car repair category now, it could (easily) lead to new debt. I’m not a sports guy, but a sportsing analogy is perfect here: Imagine a football team that’s really good at playing offense. I mean they’re killing it! But when it comes to their defense, the coach shrugs and says, “Meh, let’s just not put any players on the field.” Well, they’re going to lose, right!? And that’s just the truth. The same is true with our money. You gotta play some defense (read: avoid new debt) before you’re ready to go on offense (read: pay off debt). 3. Build Your Emergency FundIf you think about it, your emergency fund is just another one of those larger, less frequent expenses—except you don’t know what it’s for. Murphy’s Law correctly reminds us that things will happen (we just don’t know when or how much they’ll cost). Maybe your new-ish car’s battery will bite the dust. Maybe your crazy dog will impale herself with a stick (true story, my dog’s ok, thank you). Or, an unexpected global pandemic directly impacts your income (we definitely didn’t see that one coming). So should you pay off debt or save more cash? Well, here comes the drumroll… Your emergency fund should come first! You heard that right, debt—we’ll deal with you later. So, if you’re paying attention, you budget in this order:

So How Big Should My Emergency Fund Be?Some gurus say an emergency fund should be $1,000 to start, some recommend a more sizable 3-6 months of living expenses. Your emergency fund might just be whatever cash you have on hand right now. 4. When Income is Uncertain, Up Your Cash CushionIn the midst of uncertainty around income, it’s worth considering hanging on to cash—even more than you would normally. It might be more important right now to know you’re covered for a few months of essential expenses than knocking back your debt balance.

Having more cash buys more time. If you’re facing reduced income, more cash gives you more time to calmly decide what to do. This usually results in better decision making. Right now, you might be feeling a loss of control. You can’t control whether or not you’re going to lose your job, be furloughed, or see a pay cut, but having cash creates more options that give you some of that control back. This isn’t just powerful financially, but emotionally too. That’s because money in the bank is a concrete certainty, and this can be comforting. You can stretch your cash, but you can’t stretch cash you don’t have. If you’ve got a healthy cash cushion already and your income seems stable, there’s nothing wrong with continuing your debt payoff as planned. Just know it’s OK to cut back and increase your cash cushion should anything change. 5. Things Change? Change Your MindThe beauty of this approach is that by prioritizing cash, you’re not making a permanent decision. If you decide to hold off on paying debt to build a bigger cushion in uncertain times, you can always change your mind later and put that money towards debt when things get more stable. But you can’t change your mind if you put all that money on debt now. That is a more permanent decision. Still Have Questions About If You Should Build Your Emergency Fund or Pay Off Debt?If you want to learn about debt, check out our free Debt video course with short, bite-sized lessons so you can get out of debt (and stay out!). The post Which Comes First: Emergency Fund or Pay Off Debt? appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/which-comes-first-emergency-fund-or-pay_30.html October 30, 2021 at 03:42AM

Which Comes First: Emergency Fund or Pay Off Debt?

You might be asking yourself, “Should I build my emergency fund or pay off debt first?” If you’re debating between paying off debt or saving more cash, your emergency fund should come first! You heard that right, debt—we’ll deal with you later (soon, but later). See, they’re both good options, but there is a gooder, er, better option. Whenever you’re dealing with multiple financial goals, they all elbow for your attention (and your dollars). But there is a method to this madness, and that’s what I’d like to talk about today. Should I Build My Emergency Fund or Pay Off Debt First?Before we can talk about saving for emergencies or crushing your debt to smithereens, there’s the matter of your basic needs: 1. Cover Your Basic NeedsFirst things first, you have to cover your essentials with the dollars you currently have. These are things that:

Typically, they’re expenses related to survival:

And how far out are they covered? Just next month? If you’re faced with uncertainty around income, you might want to stop at this step and use your cash to cover these essentials a few months out. Once you’ve got those covered, you move on to… 2. Cover Your Non-Monthly (But Necessary) ExpensesThese expenses are the purchases that you know are coming, but they don’t happen every month. These might be things like:

When you’re looking at the total cost of a month of your life, you want to include these one-off expenses. You can think of this as preventing future debt. By breaking these larger costs down into monthly chunks, it’s not a huge blow when the multi-hundred dollar bill comes due. You’ll have the money already set aside and it won’t need to go on the credit card. Why Saving for the Basics Matters So MuchIt’s easy to see why paying our monthly bills is the top priority. You need a roof over your head, and food to keep you alive. But what about those irregular expenses? It’s harder to put aside dollars for car repairs when your car seems totally fine—especially when you’re wrestling with debt! The thing is, if you don’t fund your car repair category now, it could (easily) lead to new debt. I’m not a sports guy, but a sportsing analogy is perfect here: Imagine a football team that’s really good at playing offense. I mean they’re killing it! But when it comes to their defense, the coach shrugs and says, “Meh, let’s just not put any players on the field.” Well, they’re going to lose, right!? And that’s just the truth. The same is true with our money. You gotta play some defense (read: avoid new debt) before you’re ready to go on offense (read: pay off debt). 3. Build Your Emergency FundIf you think about it, your emergency fund is just another one of those larger, less frequent expenses—except you don’t know what it’s for. Murphy’s Law correctly reminds us that things will happen (we just don’t know when or how much they’ll cost). Maybe your new-ish car’s battery will bite the dust. Maybe your crazy dog will impale herself with a stick (true story, my dog’s ok, thank you). Or, an unexpected global pandemic directly impacts your income (we definitely didn’t see that one coming). So should you pay off debt or save more cash? Well, here comes the drumroll… Your emergency fund should come first! You heard that right, debt—we’ll deal with you later. So, if you’re paying attention, you budget in this order:

So How Big Should My Emergency Fund Be?Some gurus say an emergency fund should be $1,000 to start, some recommend a more sizable 3-6 months of living expenses. Your emergency fund might just be whatever cash you have on hand right now. 4. When Income is Uncertain, Up Your Cash CushionIn the midst of uncertainty around income, it’s worth considering hanging on to cash—even more than you would normally. It might be more important right now to know you’re covered for a few months of essential expenses than knocking back your debt balance.

Having more cash buys more time. If you’re facing reduced income, more cash gives you more time to calmly decide what to do. This usually results in better decision making. Right now, you might be feeling a loss of control. You can’t control whether or not you’re going to lose your job, be furloughed, or see a pay cut, but having cash creates more options that give you some of that control back. This isn’t just powerful financially, but emotionally too. That’s because money in the bank is a concrete certainty, and this can be comforting. You can stretch your cash, but you can’t stretch cash you don’t have. If you’ve got a healthy cash cushion already and your income seems stable, there’s nothing wrong with continuing your debt payoff as planned. Just know it’s OK to cut back and increase your cash cushion should anything change. 5. Things Change? Change Your MindThe beauty of this approach is that by prioritizing cash, you’re not making a permanent decision. If you decide to hold off on paying debt to build a bigger cushion in uncertain times, you can always change your mind later and put that money towards debt when things get more stable. But you can’t change your mind if you put all that money on debt now. That is a more permanent decision. Still Have Questions About If You Should Build Your Emergency Fund or Pay Off Debt?If you want to learn about debt, check out our free Debt video course with short, bite-sized lessons so you can get out of debt (and stay out!). The post Which Comes First: Emergency Fund or Pay Off Debt? appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/which-comes-first-emergency-fund-or-pay_28.html October 28, 2021 at 10:42AM

Slay Your Loans With YNAB’s Loan Planner

Want to find more money to pay off your loans? The new Loan Planner from YNAB can help you save time and money on your loan payoff. Loans come in all flavors and sizes. Some drive you crazy, others lurk in the corner, and some seem so large they feel like you’ll never pay them off. In the meantime, loans hold more sway at the decision making table than you’d like to admit: you struggle to save for a down payment, you’re cuffed to a job, you can’t take a chance on a cross-country adventure—all because of those non-negotiable monthly payments. Wouldn’t it just be great to dig a few holes in your backyard and BAM, you discover a treasure chest of gold coins to pay off those never-ending loans once and for all? Well, we’d like to introduce you to your shovel. We’re going to help you find more money to pay off those loans. And get this: the money is already right there in your metaphorical back yard. Say what now? We’ve all got treasure chests buried nearby? Well, not quite…but also not too far off. I’d like to introduce you to YNAB’s Loan Planner. It’s like a treasure map to find your hidden golden doubloons. Let’s get your time (and money) back in your control. YNAB’s Loan Planner: How It WorksStep One: You Acquire a LoanLoans generally originate from big expensive things that are hard to pay for in one fell swoop: think cars, college, houses, that sort of thing. To help you understand the power of the Loan Planner, we’ve got a story to illustrate: Meet Ellie. Ellie is the very proud owner of a new-to-her car. She immediately named the car Sandy the SUV, and it’s a pretty little zoom zoom with beige leather interior, heated seats, and a retractable sunroof. This car was an arrival point. She feels like an adult. While all you saw was her Instagram post holding keys next to a car with a bow, the behind-the-scenes story is that Sandy came with a price tag of $22,000. Ellie will be paying $365/month every month for the next six years to own this car (and her not-too-shabby, not-too-great credit score got her a loan with 6% interest). Ellie drives Sandy the SUV home and opens her YNAB budget. There, she adds a new loan account for Sandy the SUV.

Ok, cool, so Ellie added an account in her budget. Are you supposed to be impressed? Where are the gold coins and treasure chest? Step Two: You See Your Loan in a New LightHere’s where the magic comes in. When Ellie opens the loan account on her laptop, a screen pops up showing her a more in-depth view of her loan. She sees she’ll pay $4K in interest has has six years remaining. She’ll end up paying over $26,000 in total for Sandy the SUV. Well huh, they didn’t quite spell it out in those words at the dealership—they just highlighted the fairly reasonable monthly payment.

Step Three: You Start ExperimentingBut Ellie is curious: what would happen if she paid a little more on this loan, instead of just the monthly payment? So she decides to experiment right in YNAB: instead of simply paying the $365/month minimum, what if she tacked on an extra $100 a month? Thanks to the handy dandy Loan Planner, she sees this incremental extra would save her $1,000 in interest and shave almost a year and a half off the life of the loan.

Step Four: You Take ActionAnd here’s where it gets cool. Could she actually swing an extra $100/month? She remembers cancelling a gym membership last month and knows she has extra wiggle room. Ellie can immediately put that plan into action within her budget. Instead of budgeting $365/month (her monthly payment), she will plan on budgeting $465/month instead.

Step Five: Your Behavior Starts ChangingEllie goes about her day, zooming around in Sandy the SUV and a curious thing starts to happen—she starts making slight little tweaks to her spending decisions. A skipped coffee here, an online shopping cart abandoned there. The YNAB loan account showed Ellie that every extra $100 she can put toward her loan this month is actually worth $142.64 when paid against her loan: because she’s cutting down on the interest she would’ve otherwise paid. It makes the lure for a new t-shirt seem like a not-as-good deal for her money compared to paying off her car loan.

Are you starting to see how these golden coins could start appearing in your very own backyard? But Ellie doesn’t stop there. This month is a glorious three-paycheck month. In the past, the extra money would have been enjoyed but frittered away. But now? She’s laser focused on owning Sandy the SUV free and clear, like the wind in her hair when she’s driving around with the windows down,and oh my we’re getting off track, now where were we? Right. That extra paycheck. Getting the most bang for her buck. She sees in the Loan Planner that a one-time extra payment from her third paycheck would pay off her loan TWO YEARS earlier. Time is money, my friend. And with this plan, Ellie gets both more time and more money.

Within Ellie’s budget, she sees that ferocious blow knocked a full 10% off her total loan. And it’s only the first month!!

Step Six: You Pay Off Your Loan at Record SpeedFast forward in time: while Ellie’s original loan payoff was supposed to take six years, she paid it off in a mere two and a half thanks to a little extra awareness, elbow grease, and a trusty little budget.

The YNAB Shield and SpearThis powerful Loan Planner feature, coupled with your budget, makes up the YNAB shield and spear. While budgeting with the YNAB method acts as the shield protecting against new debt, the new Loan Planner feature acts as a savage spear to drain that loan dry. The loan payoff timeline is still totally up to you (and if life happens and it takes the full six years, then that’s ok too!). But with this tool, we’re happy to bring you the full awareness and tangible numbers of what your debt payoff dollars can actually do. And turns out this hypothetical story of Ellie and her SUV is inspired by true events. While the Loan Planner has just been launched to the public, a few people from our internal team have already been putting it to good use:

Ashley Paid Off Her Car in Eight Months!“We bought a car in January. Although we were disappointed we hadn’t saved up enough cash, we paid off our car today, just 8 months later! The new loan features made budgeting extra money toward this debt really fun and motivating!” -Ashley G, Support Specialist, Product Princess, New Mama, and Proud Owner of a Paid-Off Car at YNAB Kelly Will Pay Off Her Mortgage 12 Years Early!Or, take this story from Kelly, who increased her mortgage payment after seeing the impact of rounding up on her payments: “I didn’t realize how impactful a small change could be! We saw if we rounded up on our mortgage payment, we’d save quite a bit of money *and* time. I don’t know if I’m more excited about the $72k of interest savings or the 12 years of time savings, but I do know our future selves will thank us a lot!!” -Kelly, Product Marketing, Chicken Whisperer, Home Steader, and One Step Closer to a Paid-Off Home Mortgage

Learn how to get rolling with your loan account in this help doc, or join a live Q&A with YNAB teachers to learn how to optimize your budget for debt payoff. It turns out those forever-long loans can have a shorter shelf life after all. As always, we’re honored to be here with you on your debt payoff journey. If you’re in the middle of it, we hope this new tool can be a tasty mid-race gulp of your favorite fluorescent sports drink and a downhill stretch to give you a burst of energy and momentum. Put that finish line firmly in your sights! Want to pay off debt faster and haven’t started budgeting with YNAB yet? Try it free for 34 days, no credit card required and find more money for your payoff. Loan Planner FAQsCan I use this for my credit card debt?

Credit cards don’t function in quite the same way within your budget, so keep your credit cards off the Loan Planner for now! But if I want to, can I set up my credit card as a loan account? Loan accounts are a great way to track loans, but they are not well suited for credit cards at this time. We recommend that your credit cards be set up as Credit Card accounts in YNAB, instead. The Credit Card account type in YNAB is uniquely designed to help you record and budget for credit card purchases, and pay off credit card debt. Does this work on mobile and web? Yes, this feature is available on mobile and web, iOS and Android. However, if you want the full range of features, use this feature on the web. At this time, mobile has a limited view, and we recommend setting up your loan accounts and playing with the Loan Planner in the web view. Can I change my tracking account to a loan account? Yes! At this time, the migration process is only available on the web. You can follow the step-by-step migration instructions. Mobile users can create a brand new Loan account to enjoy this feature. If you’ve been using Tracking accounts to track your debt, you can change those accounts to Loan accounts! Before you change a Tracking account to a Loan account, we recommend reconciling the Tracking account. Bringing that balance up to date will ensure the new Loan account is accurate. Want to keep reading about our new Loan Planner feature? Check out this help doc for more info! The post Slay Your Loans With YNAB’s Loan Planner appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/slay-your-loans-with-ynabs-loan-planner.html October 28, 2021 at 07:42AM

Which Comes First: Emergency Fund or Pay Off Debt?

You might be asking yourself, “Should I build my emergency fund or pay off debt first?” If you’re debating between paying off debt or saving more cash, your emergency fund should come first! You heard that right, debt—we’ll deal with you later (soon, but later). See, they’re both good options, but there is a gooder, er, better option. Whenever you’re dealing with multiple financial goals, they all elbow for your attention (and your dollars). But there is a method to this madness, and that’s what I’d like to talk about today. Should I Build My Emergency Fund or Pay Off Debt First?Before we can talk about saving for emergencies or crushing your debt to smithereens, there’s the matter of your basic needs: 1. Cover Your Basic NeedsFirst things first, you have to cover your essentials with the dollars you currently have. These are things that:

Typically, they’re expenses related to survival:

And how far out are they covered? Just next month? If you’re faced with uncertainty around income, you might want to stop at this step and use your cash to cover these essentials a few months out. Once you’ve got those covered, you move on to… 2. Cover Your Non-Monthly (But Necessary) ExpensesThese expenses are the purchases that you know are coming, but they don’t happen every month. These might be things like:

When you’re looking at the total cost of a month of your life, you want to include these one-off expenses. You can think of this as preventing future debt. By breaking these larger costs down into monthly chunks, it’s not a huge blow when the multi-hundred dollar bill comes due. You’ll have the money already set aside and it won’t need to go on the credit card. Why Saving for the Basics Matters So MuchIt’s easy to see why paying our monthly bills is the top priority. You need a roof over your head, and food to keep you alive. But what about those irregular expenses? It’s harder to put aside dollars for car repairs when your car seems totally fine—especially when you’re wrestling with debt! The thing is, if you don’t fund your car repair category now, it could (easily) lead to new debt. I’m not a sports guy, but a sportsing analogy is perfect here: Imagine a football team that’s really good at playing offense. I mean they’re killing it! But when it comes to their defense, the coach shrugs and says, “Meh, let’s just not put any players on the field.” Well, they’re going to lose, right!? And that’s just the truth. The same is true with our money. You gotta play some defense (read: avoid new debt) before you’re ready to go on offense (read: pay off debt). 3. Build Your Emergency FundIf you think about it, your emergency fund is just another one of those larger, less frequent expenses—except you don’t know what it’s for. Murphy’s Law correctly reminds us that things will happen (we just don’t know when or how much they’ll cost). Maybe your new-ish car’s battery will bite the dust. Maybe your crazy dog will impale herself with a stick (true story, my dog’s ok, thank you). Or, an unexpected global pandemic directly impacts your income (we definitely didn’t see that one coming). So should you pay off debt or save more cash? Well, here comes the drumroll… Your emergency fund should come first! You heard that right, debt—we’ll deal with you later. So, if you’re paying attention, you budget in this order:

So How Big Should My Emergency Fund Be?Some gurus say an emergency fund should be $1,000 to start, some recommend a more sizable 3-6 months of living expenses. Your emergency fund might just be whatever cash you have on hand right now. 4. When Income is Uncertain, Up Your Cash CushionIn the midst of uncertainty around income, it’s worth considering hanging on to cash—even more than you would normally. It might be more important right now to know you’re covered for a few months of essential expenses than knocking back your debt balance.

Having more cash buys more time. If you’re facing reduced income, more cash gives you more time to calmly decide what to do. This usually results in better decision making. Right now, you might be feeling a loss of control. You can’t control whether or not you’re going to lose your job, be furloughed, or see a pay cut, but having cash creates more options that give you some of that control back. This isn’t just powerful financially, but emotionally too. That’s because money in the bank is a concrete certainty, and this can be comforting. You can stretch your cash, but you can’t stretch cash you don’t have. If you’ve got a healthy cash cushion already and your income seems stable, there’s nothing wrong with continuing your debt payoff as planned. Just know it’s OK to cut back and increase your cash cushion should anything change. 5. Things Change? Change Your MindThe beauty of this approach is that by prioritizing cash, you’re not making a permanent decision. If you decide to hold off on paying debt to build a bigger cushion in uncertain times, you can always change your mind later and put that money towards debt when things get more stable. But you can’t change your mind if you put all that money on debt now. That is a more permanent decision. Still Have Questions About If You Should Build Your Emergency Fund or Pay Off Debt?If you want to learn about debt, check out our free Debt video course with short, bite-sized lessons so you can get out of debt (and stay out!). The post Which Comes First: Emergency Fund or Pay Off Debt? appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/which-comes-first-emergency-fund-or-pay.html October 28, 2021 at 06:42AM

Budgeting for Couples When You Don’t Share Accounts

So, you’ve chosen to share your life, your space, your self, your bed, your innermost hopes, fears, successes, and failures—but you put your foot down at sharing a bank account. Hey, some things are sacred, right? Although a wise man once said, “When it comes to budgeting with a partner we take a hard line: If you’ve joined your lives, you should join your finances. Joint accounts all the way,” a truly wise man (or woman) understands that life is not a one-size-fits-all situation. (We’re the wise human in both of these scenarios. Let us have this one, okay?) If keeping the peace in your household involves maintaining separate accounts, you’ll get no judgment from us. We’ll leave that up to the disapproving family members who are all up in your business. Every family has one. We’re here to help. And to work in sly references about our wisdom. Let’s take a look at how you can make budgeting for couples work without combining your checking, savings, or investment accounts. Budgeting for Couples With Separate AccountsTo make this easier to follow, let’s take a peek at how an imaginary couple, Jamie and Jordan, manage their individual and shared finances. First, the basics. For this method, they use the following:

Yes, their financial plan comes to a total of three budgets and six accounts, not including investments. (You can see why joint-everything would be simpler, eh? Just an observation, not a judgment!). So how can they manage their household budget successfully? We’ll explain. 1. Budget Your Paychecks SeparatelyWhen Jamie gets an inflow of new dollars, they’ll be assigned in Jamie’s YNAB budget. Likewise, when Jordan gets an inflow of new dollars, they’ll be assigned in Jordan’s YNAB budget. This gives Jamie and Jordan complete control over how to assign their own dollars and should, theoretically, lead to fewer disputes about spending. When Jamie was creating a budget, she only added categories and accounts specific to her. Same goes for Jordan’s budget: it only had Jordan’s categories and accounts. These are things like their own discretionary food or coffee budgets, their own fun money, perhaps gas money, and any bills they’re solely responsible for. 2. Contribute to a Shared Account for Household ExpensesThere’s one caveat to this approach: every payday, Jamie and Jordan both agreed to contribute a predetermined, set amount to the shared household checking and savings accounts. This pays for shared expenses and helps them meet their joint savings goals. Here’s how they track this:

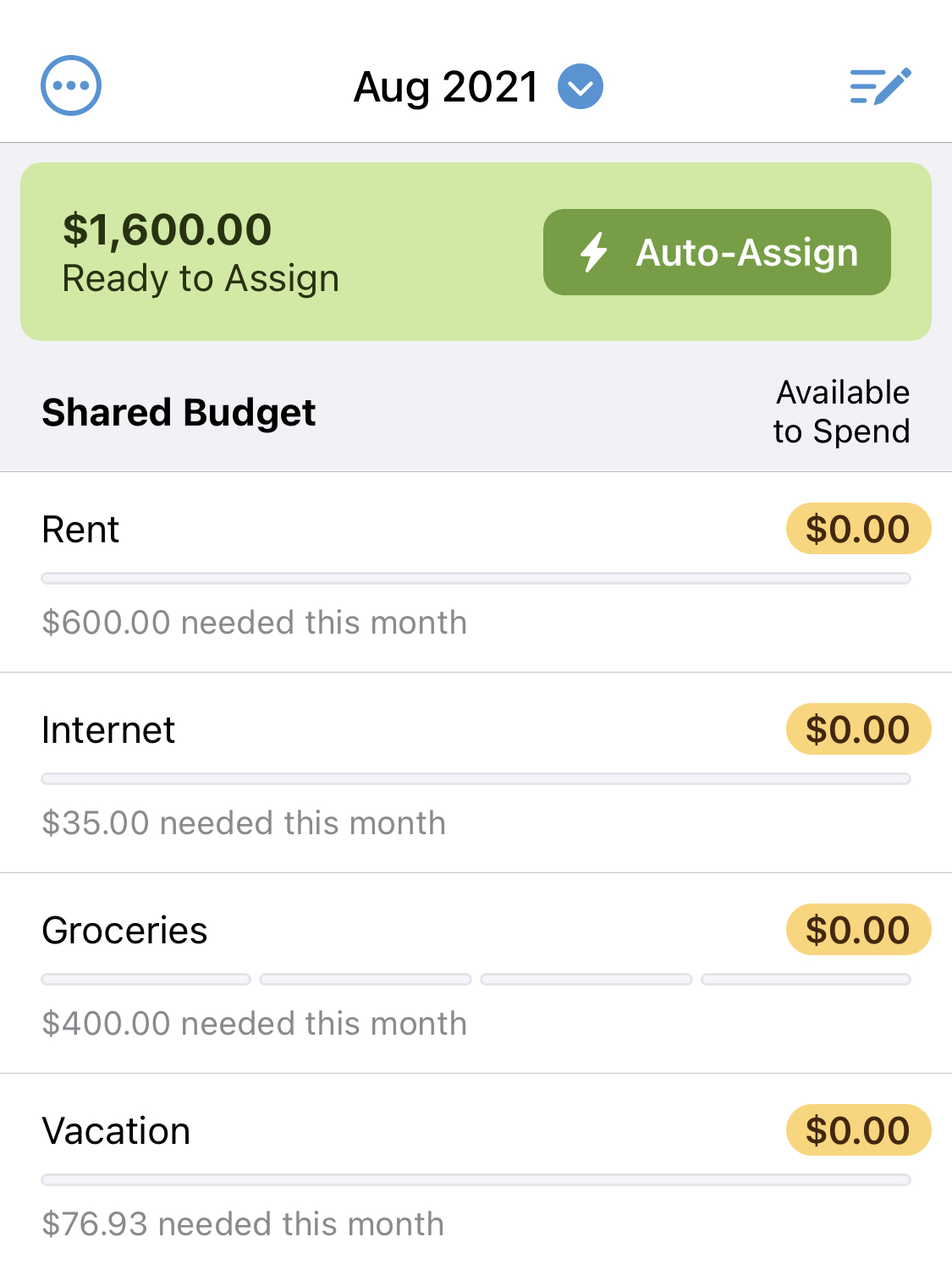

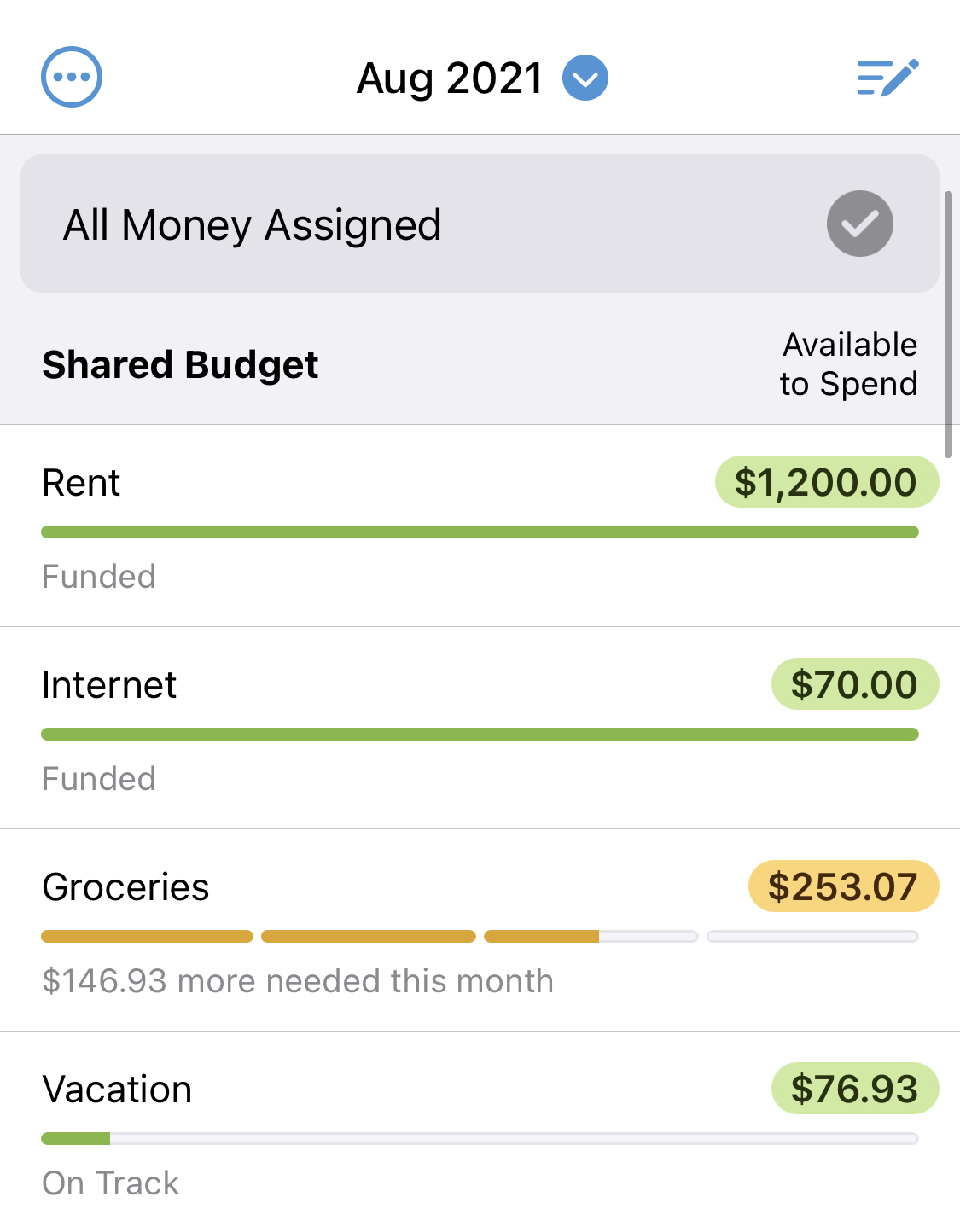

In the case of Jamie and Jordan, their contributions are equal. If one partner makes significantly more than the other, it might make more sense to contribute based on a percentage of income. This is the stuff you’ll need to work out together. You can see in their YNAB budget below, they’ve each contributed $800 for a total of $1600 to be assigned in their shared budget.

3. Budget Household Expenses TogetherThen, together, Jamie and Jordan use the household YNAB budget to assign jobs to the dollars in the household’s checking account. Those dollars cover shared bills and expenses, like the rent/mortgage, utilities, entertainment, an emergency fund, and shared food.

4. Make Decisions About Shared Goals in the Shared BudgetJamie and Jordan set up categories in their shared budget for joint goals like vacations, holiday gifts, and semi-annual insurance premiums. Together, they work together to fund those. Speaking of goals, Jamie and Jordan are wisely thinking ahead, and they’ve set up their household savings account to feed each of their Roth IRAs for saving for retirement, a tip their financial advisor recommended they set up when they asked about retirement planning. The Benefits: Individual Control While Still a Team This method may sound convoluted from a distance, but (still imaginary) Jamie and Jordan swear that it’s a cinch in practice for their personal finance setup. They also swear that the person who suggested it is extremely wise and probably very attractive. (Ahem.) They like this method because:

What You Could MissNow, I need to point out that all of the above can be accomplished (and simplified!) by using one budget and one joint-account—the benefits of which are not to be dismissed:

But you do you! I’m just pointing stuff out over here. What About Your Household?In any relationship, there’s certainly an art in keeping the peace when it comes to money differences. We’re firm believers in the power of budgeting to bring relationships even closer. As funny as it sounds, managing money and expenses has a way of aligning what matters to both of you and putting you on the same page. If you’re new to budgeting, we have a system that’s saved relationships, brought people together, and gotten couples working together to pay down debt, break the paycheck to paycheck cycle, and improve communication. Sign up for your free 34-day trial today. The post Budgeting for Couples When You Don’t Share Accounts appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/budgeting-for-couples-when-you-dont.html October 27, 2021 at 05:42AM

Do I Need a Savings Account?

There are a lot of reasons why people don’t start a budget, but I think the biggest culprit is often the perception that budgeting will take a lot of work. You’ve got to spend time thinking about your priorities (and that’s the real work), make decisions about your savings goals, and you’ve got to budget when you get paid. But the worst of it is keeping up with all those accounts, right? We find that a lot of people struggle with budgeting because they just have too many accounts to keep up with. It’s easy to reconcile one or two accounts every day, but most people have a lot of accounts. Pretty much all of us have a savings and checking account at the very least. But some have multiple checking accounts—one for bills, another for fun money, and another for everything else. Then there’s credit cards. Every company seems to be in the credit card business now, and you can’t avoid their sales pitches whether you’re buying clothes at Kohl’s or trying to get a little sleep on an American Airlines flight. And there’s always a new card offering rewards that are just a little better than what you have now. It’s no wonder we end up with so many. Savings accounts are the big culprit though. Some have six or seven of them! One for taxes, one for the emergency fund, one for that Disney vacation, that online savings account they got for the sign-up bonus, and so on. We often call this “budgeting with accounts” and a lot of people do it. Without a budget, there’s just no way to keep track of all your savings dollars other than divvying them up to an ever-growing number of savings accounts. The Cost of Too Many AccountsWhat people don’t realize is all this craziness has a cost—and I don’t just mean bank fees (which can really add up, by the way). The real cost is your time and your energy. Managing that many accounts takes a lot of both. And you do have to keep up with them, whether you’re budgeting or not. What with managing a dozen transfers every paycheck, making sure we don’t accidentally overdraft anywhere, and remembering what account is for what purpose, it can be a nightmare. So why are we, as a culture, so focused on accounts? Well, because we all need a budget, but most of us don’t have one. We all need some kind of a structure to manage our money. Most financial institutions aren’t that interested in helping people budget (it might cut back on their super-lucrative overdraft fees), so the only tool they offer to provide that structure is more accounts (which, of course, comes with more fees to pad their accounts). But there’s a better way. Trust Your Budget and Close Some AccountsYour budget can provide the structure you need, and you don’t need so many accounts. And if you’re worried about accidentally spending money if you don’t hide it away in a savings account, you don’t have to be. Your budget solves that problem too (and does a better job of it, to boot). If you trust your budget and make your spending decisions by looking at your categories, not your account balances, your budget will protect your savings dollars.

So when people avoid budgeting because they’re afraid of actively managing a dozen accounts, they’re operating under a false assumption. With a budget, you don’t need such a complex account structure. Imagine if you only had a couple accounts to deal with and your budget provided the structure you need to manage your money. You wouldn’t have to spend so much time on chasing fees and transfers and you could spend more time on what’s really important—deciding what you want your money to do for you. But Why Stop There?In fact, aside from a few situations where a separate account is absolutely necessary (HSA’s, retirement accounts, money market accounts, etc.), you really only need one account. That’s right. I’m just going to come right out and say it--if you have a budget, you don’t need a savings account at all. All your money can sit happily in your checking account while your budget keeps track of the jobs they have to do, whether that’s saving for a new car, buying groceries this weekend, or just sitting around indefinitely in case you suddenly lose your job. But what about interest? Well, yes, it’s nice to earn interest on the money you’re saving anyway. That’s why for the past 15 years at YNAB, we’ve recommended folks keep one checking and one savings account. But we’ve always dreamed of the day when we could cut that down to just one account. In fact, in a similar blog post from way back in 2010, Jesse said this: “Honestly, if I could find a checking account that paid a higher interest rate, I’d have one account and let my budget take care of everything else.” Ladies and gentlemen, for many of us, Jesse’s dream has become a reality. Many legitimate online banks are offering checking accounts with 2.25+ percent interest rates (at the time this blog was written). SoFi and Aspiration Bank are just a couple of the more-popular options not to mention a host of smaller, regional banks and credit unions that can sometimes do even better. Now, these may not be right for everyone, but they could be just right for you. I myself just opened one of these high-yield checking accounts and I’m very excited to finally achieve the ultimate YNAB goal of having just one account for all my savings and checking! So what about you? Is your account structure giving you a headache? Why not start by closing just one account today. And if you do, let us know on Facebook, Instagram, or Twitter. We’d love to hear from you. The post Do I Need a Savings Account? appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/do-i-need-savings-account.html October 26, 2021 at 05:42AM

Using Data To Make Winning Investment Decisions

There is a tremendous amount of data that can help you make better investment decisions. One strategy I used was the FS20 guide for property buying. Another interesting data source is the Yelp Economic Average report for buying stocks. Let's discuss! Posts mentioned: The FS20 Property Indicator For Buyers Health And Fitness Stocks: The Last Reopening Trade

via Blogger http://shandradotson.blogspot.com/2021/10/using-data-to-make-winning-investment.html October 26, 2021 at 03:42AM

What is a Sinking Fund & How To Set One Up

What is a Sinking Fund?A sinking fund is a fixed amount of money you save each month to prepare for a non-monthly expense like a car repair, or a twice-a-year insurance payment. (Side note: Sinking Fund would also be a great name for a boat. I might add that as a wish farm goal.) Anyway, I know the car will eventually need repairs. We all know that. Although it always feels like a surprise when it happens, it’s actually a known expense. How much will these repairs cost? I have no idea (hopefully very little). I know that our life insurance premiums are due annually. It’s a known expense. How much will the premiums cost? We have term insurance, locked in for at least a decade, and it comes to $840 per year. Some other common examples of sinking funds are home repairs, medical expenses, vacations, Christmas gifts, building an emergency fund, or even an Amazon prime membership. See a list of other sinking fund categories you might want in your budget! How Much Should I Set Aside in My Sinking Funds?Based on past experience, let’s say we spend $2,000 per year on car repairs. That means I need to be socking away $167 into my Car Repairs savings account (or YNAB category, but we’ll get there). For the life insurance premium, $70 per month means we’ll be able to pay for that premium easy-breezy. Why Do I Need a Sinking Fund?Picture this: you open your mailbox, see a bill, and all of a sudden you need $700 for a car insurance premium! If you don’t have the money, what’s the first thing you do? Pull out your credit card, and into debt you go! It’s disheartening, to say the least. But how about this instead of borrowing money, you just set aside a manageable amount for a number of months to reach your goal. The bill arrives, and you have money sitting there ready to pay for it. Yes, it’s utter bliss. Already have a sinking fund? Well, consider it a badge earned on your sash of personal finance accomplishments. Want one? Keep reading, we’ll tell you how to set one up. How Do I Create a Sinking Fund?How do you start establishing a sinking fund? Some non-YNABers advocate setting up a separate checking account or savings account and then keeping a lot of separate “accounts” within that checking account for all of your Sinking Funds. If it’s a large amount of money for a long term expense (say, for a new car or a down payment on a house), it can be beneficial to save money in a high yield savings account or money market fund to take advantage of higher interest rates. This can be a great setup, but depending on your bank, it may be a little complicated to get just right. Instead of having 24 different bank accounts for all your savings goals and financial goals, we set up ours in a YNAB budget (see an example here), which gives an all-in-one view that feels a whole lot simpler to manage. The beauty of the YNAB system is that all of these accounts can be easily managed right in your budget. When you’re setting up a sinking fund, you just create a Car Repairs category in YNAB, and then you just “sink” or set aside money into it every month and watch the balance rise. In order to keep the number of physical accounts down at our household, I only use a separate account for our New Car Fund (I wish). All of the other accounts are small enough that I don’t bother earning any interest. It’s your personal call though. At the end of the day, implementation details aren’t the important part. What’s important is that you’re looking ahead and actively planning what your money is going to do and when. You’ll then find that all of those “emergencies” that used to knock you off your financial feet are now not a problem at all. Expect your “unexpected” expenses by setting up a sinking fund to pay for them when they pop up. Want to start getting ahead of your bills instead of constantly playing catchup? Start your YNAB budget to streamline your sinking funds and simplify your financial life. Try it free for 34 days! The post What is a Sinking Fund & How To Set One Up appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/what-is-sinking-fund-how-to-set-one-up.html October 25, 2021 at 11:42AM |

RSS Feed

RSS Feed