|

Budgeting When You’re Barely Getting By

It can be tough to figure out how to budget when you’re broke. Not only are you trying to adopt a new habit, you’re also learning a new method of managing your money, figuring out the technology of a new app…and you still have to go to work, feed the kids, clean the house, and find money for the next bill. Enter: a pounding, stress-inducing headache and a strong desire to avoid reality. Hold on a second. Deep breath. You’ve got this! And doing it will ultimately make your life easier. Let’s get started. How to Budget When You’re BrokeLet’s walk through what you can do—right out of the gate—even if you’re short on cash. Step #1 : Rearrange your categories to better match your priorities.Here’s an example:

The first group “Must” include fixed expenses. These are the bills that I know are coming. They absolutely have to be paid and I have a pretty solid idea of how much each will cost. The second group “Need” is for variable expenses. These are the expenses I do know are coming, but I either don’t know when, or the amount varies. For example: Auto Maintenance. If you’ve got a car, it’s not a question of if it needs work, just when and how much. The final group “Want” is optional expenses. These are the categories I hope I can budget for, but if things are tight, they may get put on the back burner. I don’t need to buy music right now. I hope to, but I can skip it if things are tight. Not sure how to change categories? Watch this video to learn how. Step #2 : Set up scheduled transactions.The fixed expenses are probably the bills you dread most right now. Just when you get some breathing room, another one shows up to bite! But there’s some good news: these bills are predictable. We can spot them coming and get our budget ready to fight back. Here’s how: set up scheduled transactions for each bill. YNAB will enter these transactions into the register on the scheduled date and reset the scheduled transaction to the next occurrence.

Because I added those scheduled transactions, if I look back on the budget I can see those orange alerts reminding me of the bills that are coming.

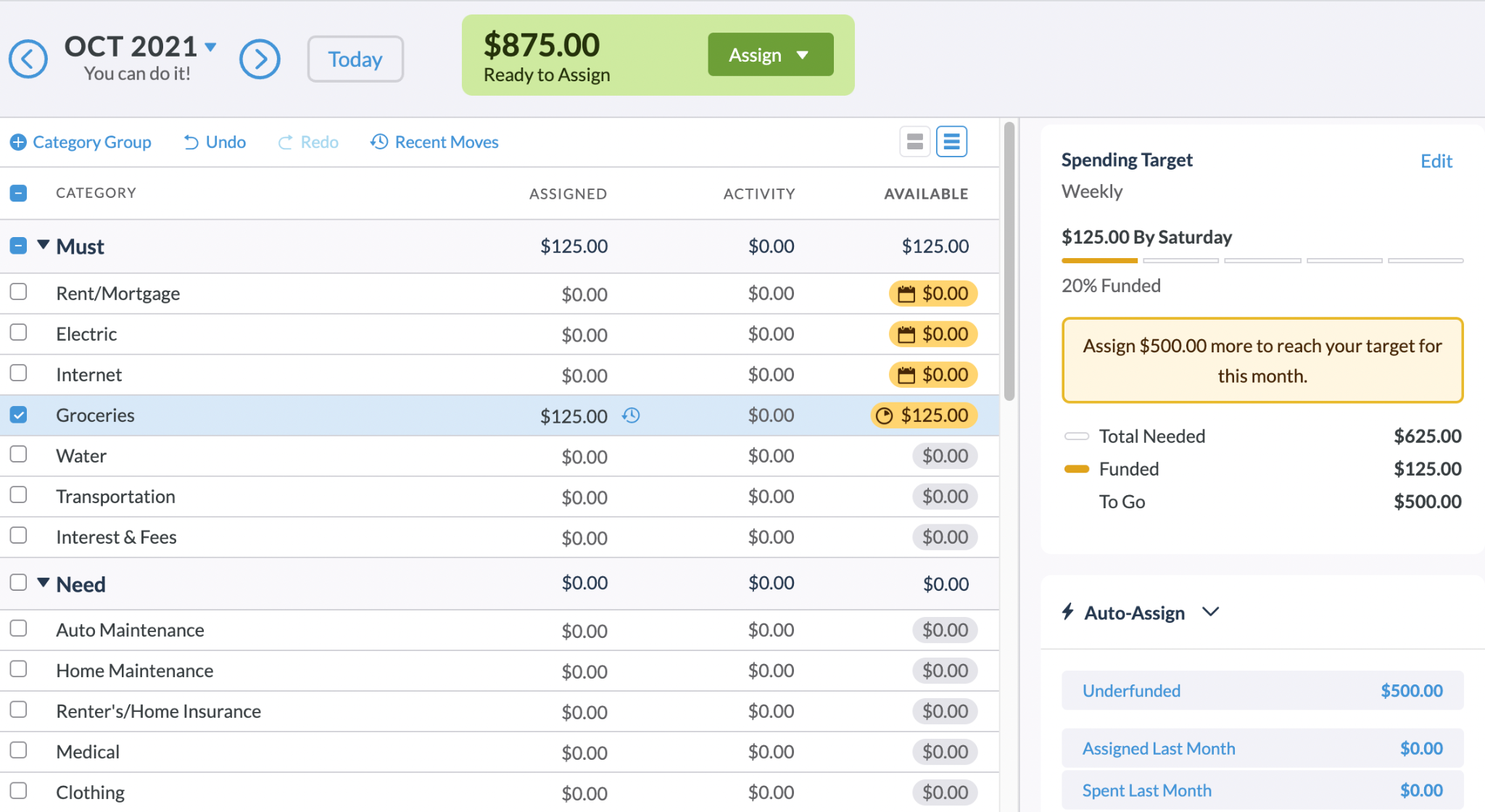

You can also drag your categories into the order they fall in the month. That way, when money arrives, you can budget your way down the screen. Here’s how to set up a recurring scheduled transaction. Step #3 : Add a target to each remaining Category.Targets can help alert you about how much you need to fund other categories. I’ve added a weekly target to groceries, because I want to be reminded that I need to budget that amount for groceries.

To create spending and savings targets, just click on the category, select “Create Target” and decide how much money you need and by when. You can choose to create three types of targets:

Now as you do this, you may find that for some of your categories, you have no idea how much to budget. Don’t worry about that. Just guess. Most people guess when they get started; you’re starting a budget, not chiseling commandments into stone. You can always make changes later. So go ahead—turn those guesses into targets. Learn more about how to set up targets in your budget. If you select all the categories that have a target or scheduled transaction attached, you’ll see a total on the right-hand side in “Underfunded”:

That’s what you need to bring in to cover all those categories. If you know you’ll bring in less than that, start making adjustments to the targets where you can. If you bring in more than that, you can start working on the optional categories. Step #4 : Budget the dollars you have.This is where it gets stressful when you’re figuring out how to budget when you’re broke. Although it can feel overwhelming to make decisions when you don’t have enough money to cover everything, you need to make a very clear plan for the dollars you do have. If you only have $148, it’s absolutely critical that you manage that money really well. Here’s the question you need to answer: What does this money—this $148—need to do before I’m paid again? Answer the question, and then assign those dollars where they’re needed most in the budget. When you realize your money is a finite resource and you name one job—and only one job—for each dollar, the money starts to feel a little bit scarce. Don’t panic! Scarcity is actually a good thing—it gives you clarity. You’ll start noticing as you give every dollar a job that there really is a limited number of them at any given time. That’s definitely a bummer, but it’s also the reason you need to be intentional about prioritizing what the money you have right now is going to do for you. Doing that helps build awareness and can prevent you from making costly mistakes. Every time you spend a dollar, you’re making a choice. There’s power in that. Be the boss of your money. Step #5: Track your spending.Now that we’re organized and aware of what we have, and we’ve given every dollar a job, we need to stay completely on top of spending. That’s where things can go off the rails if you lose this awareness. We need laser focus. Before you spend, check the category to see what’s in there. Don’t look at your checking account balance—that doesn’t tell you anything about what these dollars are for. You need the budget for that. Let’s say you absolutely need $35 for gas. There’s no way around it. You check your Transportation category and, yikes, there’s no money there. The first step would be to check your other categories to see if you could “borrow” the $35 from one of those. We call that WAM-ing here at YNAB, because we love acronyms and because sometimes budgeting is like one big game of Whack-a-Mole where you have to quickly slam down unexpected expenses that pop up. But sometimes the reality is that you absolutely need $35 for gas and you absolutely don’t have $35 for gas. Maybe you end up overdrafting your account and spending money you don’t have yet as you work your way through this. It’s easy to feel frustrated, or even ashamed, about overdrafts, but it’s more important to face the reality of the situation. So, you’ll still record this spending in your budget—after all, it did happen. You’ll be overspent in your gas category. And that’s true, even if seeing those numbers in red hurts a little bit. You also may have to add an overdraft fee to your “Interest and Fees” category (and, ouch, those hurt). However, you want to record what happened so that you have accurate information. When you get paid next, first budget to cover that overspending. It’s worth mentioning that if you’re in this situation, you should strive to spend as little as possible—only spend what’s absolutely necessary. Those little cheap treats you buy impulsively to cheer yourself up are only a temporary cure. Let that money add up to something more significant. Repeat steps #4 and #5.Let time go by. This might be the hardest part, but these steps will bring progress. Money will come in, you’ll give each dollar a job, and you’ll check your budget (not your accounts) to make your spending decisions. You’ll start to feel less like you’re floundering and more like you’re in charge of your spending. And believe it or not, you’ll start to like budgeting. Or at least not dread it. You’ll see it as a tool for feeling in control, organized, and capable. You’ll be able to buy those little treats when you want to because you’ll know you can afford them. Your feelings of guilt or anxiety about spending will gradually subside. It’s worth it. Hang in there—being broke is a stressful time. But you’re here, looking for another way, and you’re rewriting your story right now. Keep it up and you won’t be budgeting while you’re broke for long. (Because you won’t be broke!) If you want extra support, check out our free live Q&A sessions where a YNAB teacher can help with everything from setting up a credit card in YNAB to breaking the paycheck to paycheck cycle. The post Budgeting When You’re Barely Getting By appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/budgeting-when-youre-barely-getting-by.html October 06, 2021 at 05:42PM

0 Comments

Our DIY Heat Pump Install – Free Heating and Cooling for Life?

To most of the Internet, Mr. Money Mustache is known as the quirky early retirement financial guy, and this is a blog about Money. But really, I’m not a finance guy – someone who devotes most of his time to optimizing money. I’m more of a general Life Engineer – someone who tries to optimize everything that is fun and interesting in life, and money is just one of those things. Optimizing means getting the most good out of something – whether it is money, time, health or happiness, while minimizing waste. This is what allows us to make win/win decisions (for example things that make you richer and healthier and happier), rather than win/lose compromises (giving up something you actually like, just to save or earn more money) One of these win/win things for me has always been optimizing my own houses and buildings to be more comfortable and stylish, while costing less to own and maintain and heat and cool. After all, out of all possible decisions, your choice of home may have the biggest effect on both your financial and emotional wellbeing. Get a reasonable house that is close to your friends and your work, and you’re off to a great start. So anyway, this past summer all my favorite factors of optimizing, learning, effort, saving shit-tons of money and reducing loads of waste and pollution came together in the form of a DIY Heat Pump Installation on our commercial building downtown, the home of MMM HQ Coworking. Why Are Heat Pumps Super Exciting? Heat pumps are a technology that has recently jumped into prime time and are about to change everything about houses, just as the iPhone did to the tech industry about twelve years ago and just like electric cars are doing to transportation right now. The reason is that they have these fundamental advantages:

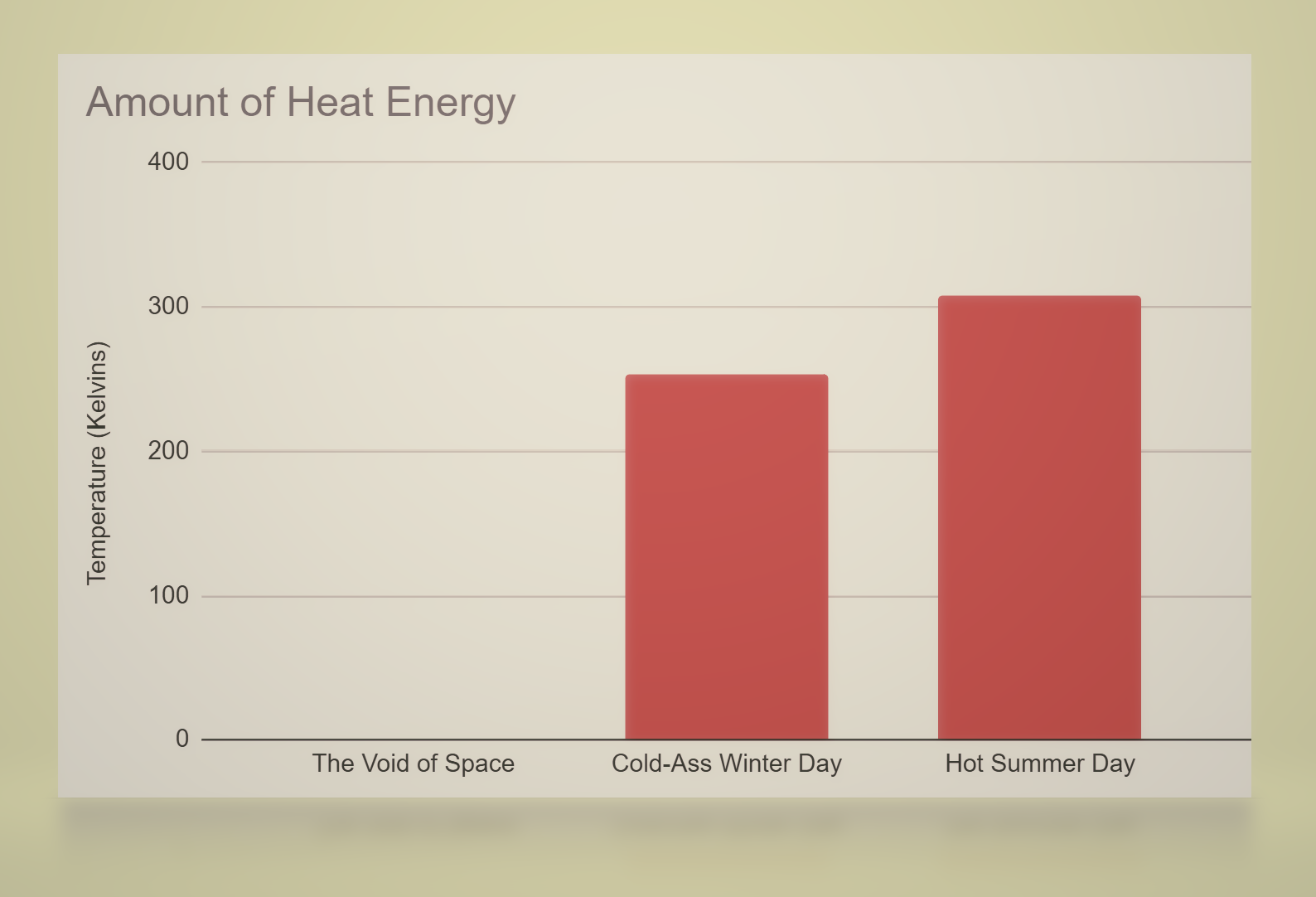

How Does a Heat Pump Magically Suck Heat Out of Cold Air? Heat pumps save money and energy because they aren’t generating heat directly like an old electric baseboard heater. They are mostly just moving heat around – from inside to outside in the summer, and from outside to inside in winter. To many people, that second situation sounds like magic, but that’s just because of our skewed perception as human beings – a creature that evolved in the warm tropics of the planet Earth. Really, there is plenty of heat even in winter air – if you view it from the Eyes of Physics:

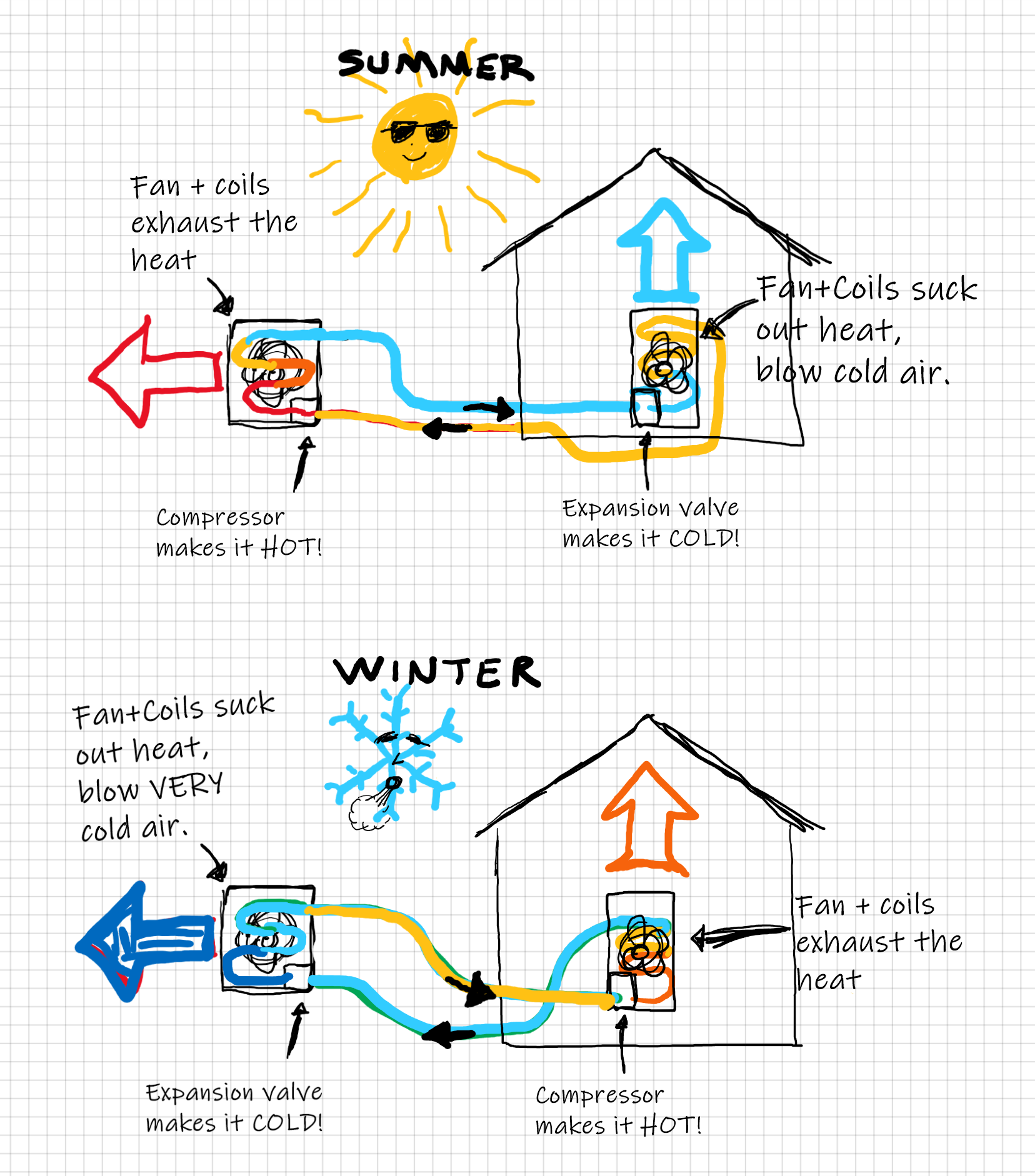

So, a modern heat pump can easily suck loads of heat even out of air that feels cold to your skin. It does it like this:

You know what else does this exact same trick? Your own FREEZER! Those things typically maintain an inside temperature of about -10F, which means that somehow it is sucking heat out of the air even at sub-zero temperatures, pumping it out to the coils underneath with a fan blowing past them. And if you put your hand there to feel that airflow, what do you feel? Warmth! Show Me The Money

Before we get into the real details, check out the quick numbers for the heat pump I just installed. Note that I live in Colorado, which has lots of heat and a moderate amount of cold – right about what you’d expect from our position halfway between Maine and California.

Annual return on investment (ROI) rate: 15% . Even better: That $275 annual figure for our electricity consumption is what we would have paid, if we had to buy all our electricity off the grid at 10 cents per kWh. But since we generate a surplus of power from our DIY solar array, our net cost is much less than that. You could even say that all of our heating and cooling is “free” on an ongoing basis, although we did spend $5000 to build the 5.5 kW solar setup in the first place. So Is A Heat Pump Really a Do-It-Yourself Project?

In a word: Yes, if you are a fairly competent do-it-yourselfer, and you choose a DIY-friendly heat pump kit. It is considerably easier than installing a gas furnace or a metal roof, but not as easy as putting together IKEA furniture. Our first install took about 16 person-hours of work for the main job (two people working a full day). Plus I spent about another sixteen dusty hours upgrading the duct work and building custom metal shapes to route the air because our coworking building was so old that the original asbestos-and-mouse-shit ducts were just not worth keeping.

The value of doing it yourself is that furnace work is one of the biggest returns on your time as a homeowner. Where I live, even a gas furnace + air conditioner replacement can cost $10,000. And although a heat pump hardware only costs about the same amount as conventional furnace+AC ($4000), the companies like to charge more for the newer stuff (or even worse, try to convince you that you’re stupid for even asking about it!). In other words, even conservatively speaking, for a basic installation you are saving about $6000 in exchange for doing that 16 hours of work, which amounts to a solid $375 per hour.

But Wait! Don’t forget about Rebates!

Even if you’re not a tinkerer, there are some good programs out there that will help subsidize the cost of an upgrade like this. The US EPA offers federal tax credits for lots of things including heat pumps, and local agencies have their own programs – for example neighboring Fort Collins will chip in $2200 towards a unit like ours, which could cover most of the cost of a professional installation! . So if you are ready to upgrade to a heat pump, you either need an honest HVAC company who will install a reasonably-priced machine for you and charge you a reasonable hourly rate. Or, you need to flex your Money Mustache Muscles on the project and do it yourself. Of course, I chose the latter approach as always, so let’s get into the details of or install! Step One: Pick a Heat Pump

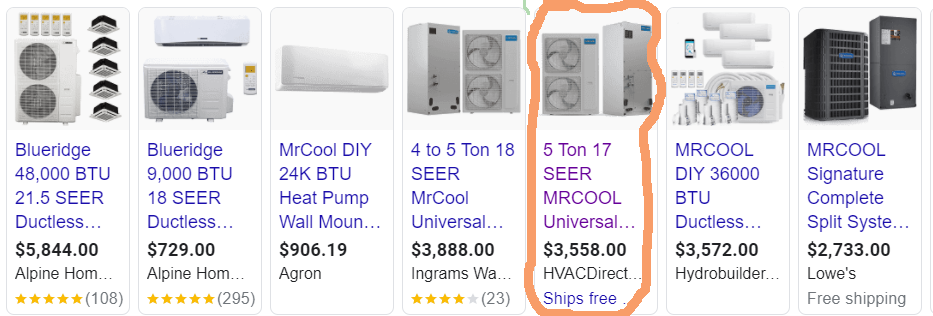

There are two things you’re looking for here: physical size and heat output. The size and shape of indoor portion (the air handler) of the new system have to be similar to your old furnace, or you need to have a plan for how to adapt the new one to blow into your old pipes. As you’ll see below, I chose to do the adapting. As for the heat output, old furnace was a “100,000 BTU” unit, which is a measure of the amount of natural gas it can suck in and burn each hour. Since it was only about 75% efficient, the heat output was about 75,000 BTU (the real units here are the archaic “British Thermal Units Per Hour”, but all you really need to know is that this is still more than enough to keep our leaky, sprawling 2400 square foot brick building warm easily through even the coldest winters.) In the most extreme situation (for us this would be a 24-hour period where the temperature is barely above 0F, and it typically does happen at least once every few years), I measured that our old furnace was running for about 8 hours per day, which means our average heat loss was about 25,000 BTU on a continuous basis (75k multiplied by ⅓ of the total hours in a day) On the cooling side, we had virtually no air conditioning. Just a few crappy portable units scattered throughout the building, with a total combined cooling power of about 20,000 BTU. This wasn’t quite enough to beat the heat in the event of a fully occupied building on a 100F day. The solution for me was thus pretty simple: the biggest Mr. Cool “Universal” combined heat/cool system, which I started conveniently seeing Google ads for everywhere once I started my research. This beauty is good for about 60,000 BTU of both heating and cooling, which could also be expressed in the even more archaic form of “5 tons”

So I bought the circled option above. In my case, I placed the order through Home Depot website, with the free “ship to store” option, but you could also try your local Lowe’s, Alpine Home Air is good, and Ingrams now sells this unit (including the required 25 ft lineset) through Amazon. Step Two: Remove your old furnace

Safety tip: Make sure you turn off both the gas and electric supply to your furnace before messing with it, as well as opening some windows and running a fan to clear out any remnants of gas as you disconnect pipes. But once you have it safely disabled, it is as simple as carefully un-wrenching, unscrewing, and cutting away parts of the old furnace (while carefully preserving your existing ductwork) until you have the old one fully removed. You can sell or give it away on Craigslist, or drop off for free at a metal recycling facility.

Step Two: adapt the ductwork as needed

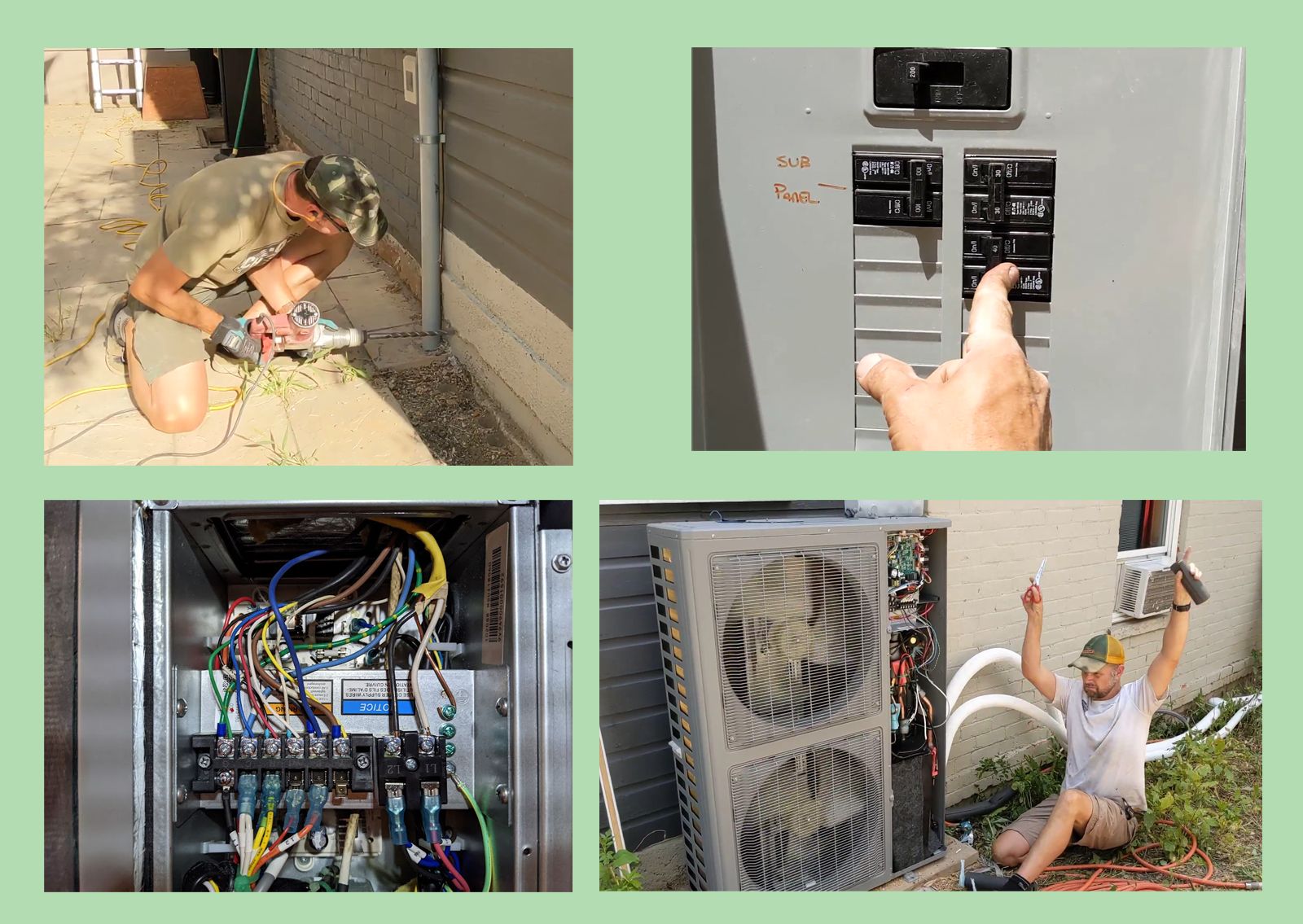

If you’re lucky (the old furnace and new heat pump are almost the same size), this step will be easy. You just connect the return ductwork to the bottom of the machine, and the supply ducts to the top. However, I was not lucky. Because our basement ceiling is so low, I had to install the heat pump horizontally (it is designed to allow this), and then build some adapters to allow the air to flow the way I needed. On top of that, most of our ducts were falling apart and poorly shaped and useless – so I repaired or replaced a bunch of them while I was in the process. This took a lot of work, but my biggest allies were a huge roll of wide, reinforced silver tape, and simple sheet metal tools like shears, angle grinder, self-piercing screws, a good breathing mask, headlamp and work gloves.

Step Three: Fit in the new heat pump

Aside from the fact that the thing is heavy (ours was around 250 pounds), this connection is surprisingly easy once you have the ducts ready. You just screw and seal the sheet metal boxes to the bottom and the top of the heat pump. And at this point, you should be getting excited because the end is in sight. Step Four: Place the Outdoor Unit Where You Want It Since the outdoor unit is another 300 pounds, you’ll want a high quality dolly and some ratcheting straps, as well as a strong friend nearby to help you wrangle it into place. Your goal is to put this thing somewhere beside your house that is out of the way, but also close to wherever you just put the air handler in the basement. Then you need a lineset that is long enough to connect them together – and shorter is generally better for both cost and performance reasons (we used a 35 footer). We put our condenser on a couple of sturdy, level concrete pads. Step Five: Run the Lineset

The lineset is a pair of flexible copper tubes that are wrapped in insulation. They are bulky, so even our 35-foot set came in a BIG roll the size of a big-screen television box. You need to carefully unroll and straighten it, and feed it in through a roughly 4” hole you drill in the side of your house so you can connect the condenser outside to the air handler unit inside. We had the added challenge of having to punch through an eight-inch-thick BRICK WALL, so I had to spend some good workout time wrestling with this massive concrete core driller, mounted to a high-torque low speed drill.

Once the lineset is in position, the connection is refreshingly easy: you carefully follow the instructions to tighten on the right nuts with a wrench, open some valves with an alan key, and you will hear the refreshing PSSSSssssssshhhhh as the refrigerant is released into the system. (This is the part that an HVAC technician would normally have to do, Mr. Cool gets around the issue by using special valves and having pre-charged linesets. More expensive, but very much worth it for the time and labor savings!) Final Step: Run the Electrical Wires

This will vary depending on the system, but ours called for the following wiring, which I subcontracted out to my partner Mr. 1500:

The Victory Lap: Fire It Up!

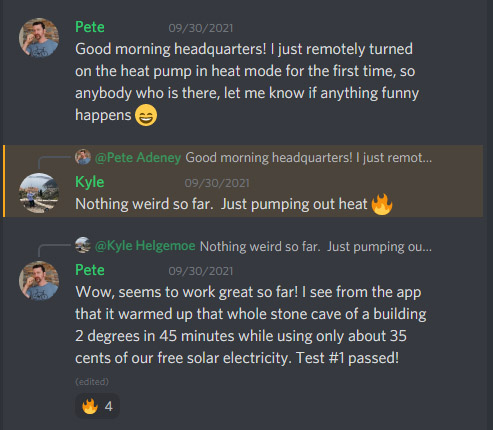

We cranked through all of these steps carefully and then flipped on the breakers with great fanfare: SUCCESS! – The Ecobee lit up and started guiding us through its setup screens. Once complete, we slid the desired temperature way down in hopes of experiencing some much-needed Air Conditioning on this hot July day. And nothing happened. We ran out to the outdoor unit and found it was just sitting there, with LEDs illuminated but nothing else happening. We both started sweating bullets. Had we made a foolish mistake and bought a faulty unit? Did we screw something up in the install? Nope – it turns out there is simply a three-minute delay between that first activation and the time Mr. Cool starts his cooling. Very slowly and with great grace, the big fan blades began to rotate, graaaaadually speeding up, with the hum of the compressor so quiet in the background that I had to press my ear up to the thing just to verify that it was really working. But boy was it ever working – we ran inside and found that that icy cold air was just blasting out of each of the seven large vents spread throughout our building, and baking hot air was now shooting out of the outdoor unit. We had instantly beat the summer heat and everybody inside raised a cheer to this new luxury. Epilogue, Three Months Later: How Well Does It Work?

Throughout the rest of the summer, we have had a lot of fun putting this system through its paces, and it has proven itself to be an incredible cooling machine. We had several events with over fifty hot bodies packed in for some of our entrepreneurship and social gatherings while outdoor temperatures were in the 90s – and we were able to maintain comfort effortlessly. The next test will of course be the winter. Here in early October, we have just turned the corner where the building has required just a bit of heat to start some mornings. With a few taps on the Ecobee phone app, I was able to flip the system over to heating mode and give it a whirl. It worked great – heating the building quickly and quietly.

But I’ll update this article over time as we move through cooler seasons. I expect it to continue to perform just great – but it will be fun to verify and reassuring to skeptics out there once we see it with our own eyes. Extra Cool Detail: How Much Electricity Does It Use?

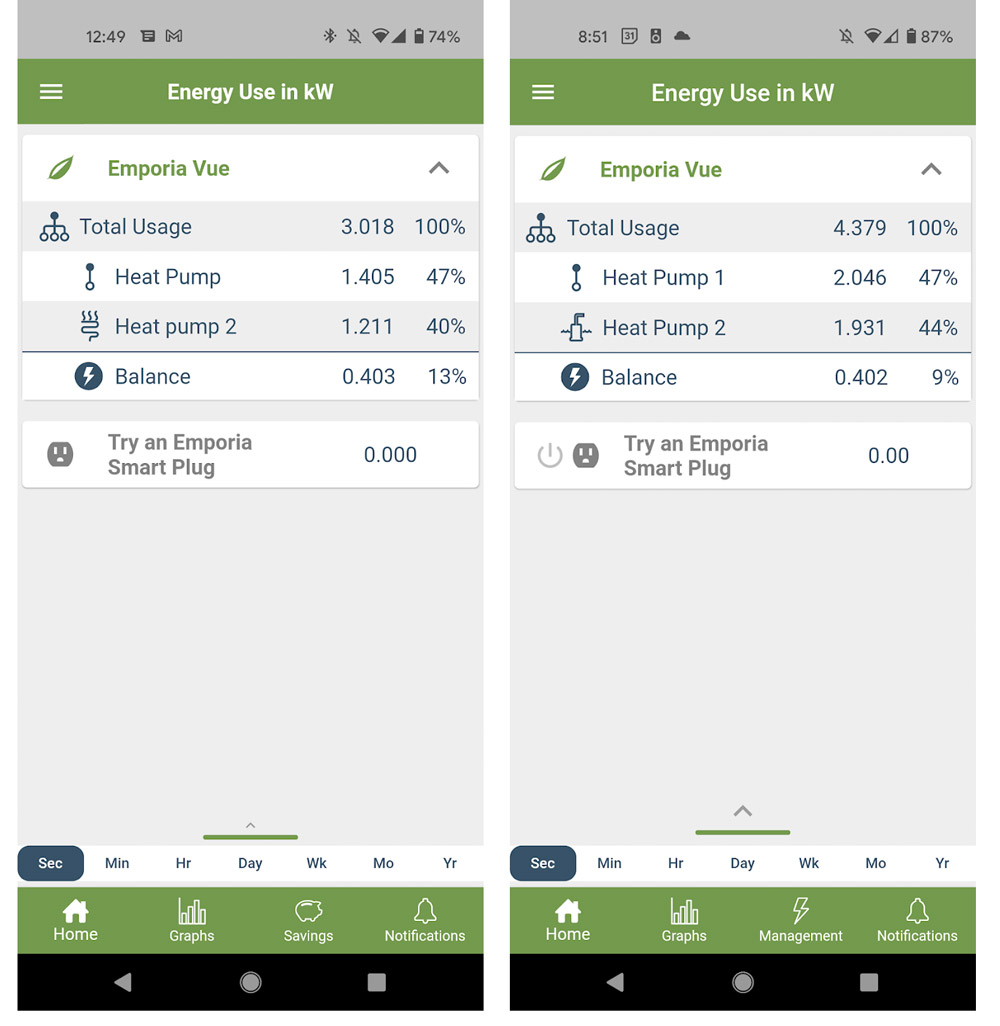

Of course, being MMM I was not content to just sit back and soak in the cool breeze of accomplishment just yet. I needed one final bit of data – a record of just how much energy this heat pump was sucking down in both heating and cooling modes, so we can get a better estimate of how much money it is saving us over the years. So I installed a system called the Emporia Energy Monitor into the circuit panel, which is currently the best value on the market for such a well-designed gadget. This allows me to track and record the full details of the energy flow – through every circuit in the house if I choose to do so. For now, I just have it watching over the heat pump. What I found is that in cooling mode, the Mr. Cool uses about 2600 watts on an ongoing basis (about the same as two large window air conditioners), which translates to 26 cents per hour of electricity. On the hottest days with the most people, I found the system ran about six hours, meaning our peak electricity use was only about $1.50 per day! To me, this was pretty remarkable – this was a 95 degree day with 50 people in the building, roughly equivalent to trying to cool a mid-sized restaurant in Texas. Yet even if we repeated this extreme situation every day, we’d rack up an air conditioning bill of only about $45.00 per month! I found that the heating mode was a bit more thirsty, with consumption at 4000 watts, or 40 cents per hour. Based on my earlier estimates of heat loss on the coldest possible days, we could be in for about 18 hours of runtime per day, which would be $7.20 of electricity. So, if the Headquarters were moved to an extremely cold climate and plunged into neverending 0F / -18C conditions for an entire month (which would make it colder than Duluth Minnesota or Ottawa Canada), we’d still face a heating bill no higher than $210 for the month. But in more realistic conditions for Colorado, we would expect about half of that level of energy consumption. And of course this is only for the month or two of our short cold season. For the rest of the year, heating is even easier. Conclusion: Heat Pumps Are The Bomb So there you have it: we dreamed about it for years, finally did it, and I could not be happier. It is such a joy to not even have an account with the gas company, and to know that this part of our expenses will be zero, forever. And of course it’s even better to know that even the electricity cost numbers in this article are just for your own comparison – in reality, we make more than enough solar electricity run this whole thing for free just from the pretty squares of black glass on the roof. Free heating and cooling for life, with no pollution (with free operation of our laptop computers and beer fridges, and free charging of our electric cars to boot) – This truly is the way of the future! In The Comments: Do you have any questions about heat pumps or other home efficiency products? And if you have a heat pump of your own, what do you think of it? Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/our-diy-heat-pump-install-free-heating.html October 05, 2021 at 10:42AM

See My Budget: I’m Living Full-Time in an RV

Want to dive into full-time RV living but wondering the details of the financials? See how a full-time RVer traveling the country is making the most of her monthly inflows without sacrificing her financial goals. About

Income: $89,000+/year (variable depending on business)

Savings: $53,000

Debt: $62,500

I debated paying off my loans when the house payment came in, but after talking to a wise friend, they said it might be nice to keep my options open with that cash. So, I see it as FU money—it’s a year’s worth of expenses. My side hustle is doing well and this might allow me to go full time. Average Monthly Inflow: $5,000+/month

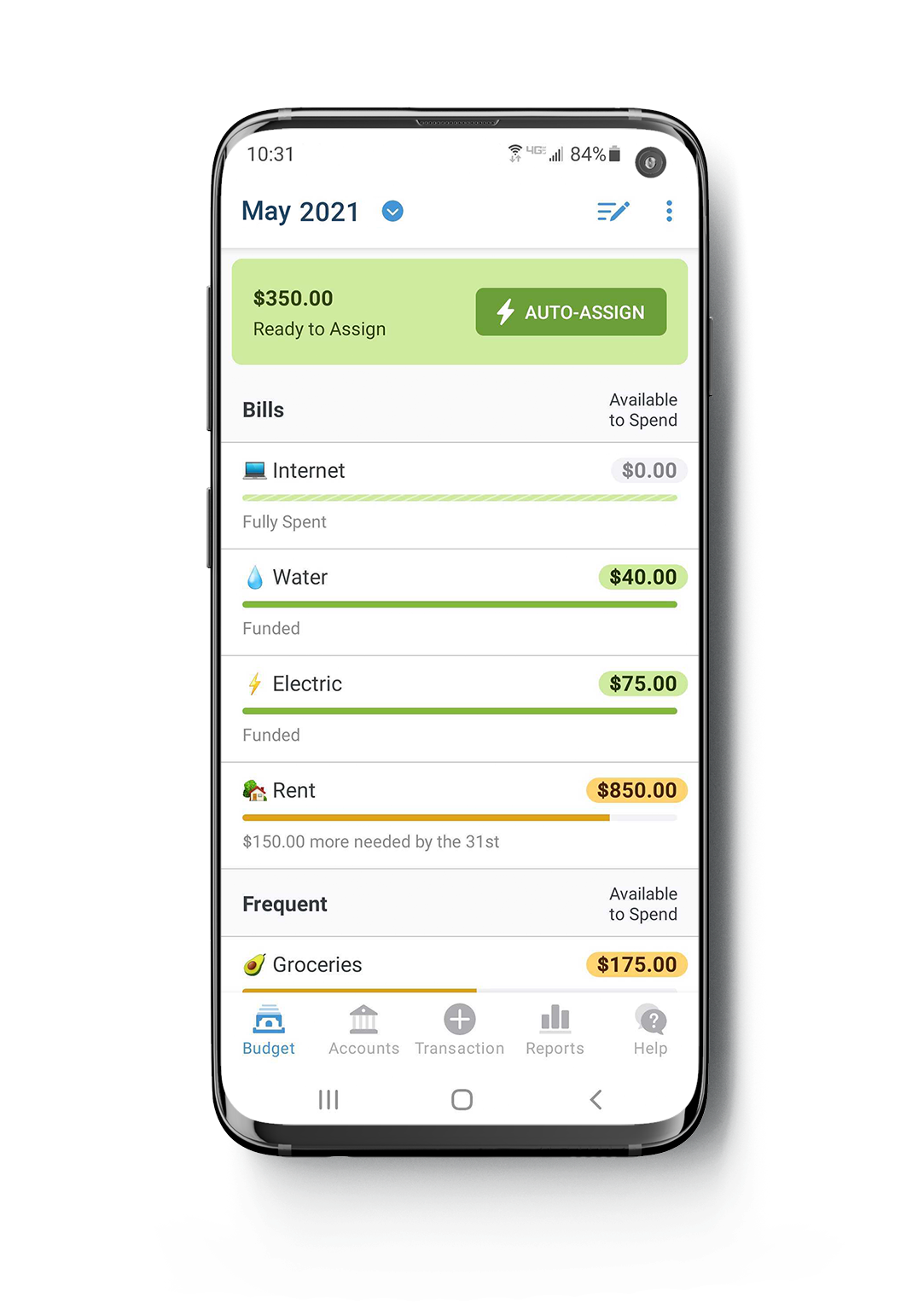

My BudgetI’ve been a YNABer since March 23, 2020: the day I moved out. I’ve got a lot of categories, but I like having them all split out so I can see how costs are broken down. Budget

Expenses Specific to Full-Time RV LivingThere are a bunch of things in my budget specific to full-time RV living:

My StoryIn late March 2020, when the world was shutting down, I finally called it quits on my marriage. Best decision I will make in my life. There were a lot of issues in our relationship, but the worst to me was his total disconnect and denial about spending within our limits. In five years, we spent $115k more than we brought in—burning through my $75k in pre-marriage savings and accruing $40k in credit card debts. I moved out with less than $400 in the bank, almost $20k on credit cards (we split the $40k credit card debt equally), and assumed the responsibility for the loan on our one-year-old RV. He kept the house, the car, and the majority of our stuff. I just wanted out. My plan was to move into the RV and travel the US seeing National Parks. In addition to the debt I already had, I had to buy $37k worth of a big diesel truck to make those dreams happen. I also needed to build an emergency fund. I work for an educational non-profit making $66k/year and I get $1,100 a month in Veterans Disability Pay. That’s less than $4,800 a month in take-home pay. I wasn’t even making it paycheck to paycheck. RV life isn’t cheap if you are on the move, so I cut my expenses down to the bare bones to make ends meet and started hustling hard:

With all that hustling and scrimping:

Between my hustling and the house settlement, it’s all about $87,000 total between paying off debt and cash saved since the divorce. That’s not counting my retirement funds, where I unintentionally managed to max out my 403b last year. Combined with a truly bumper year on the stock market for me, those accounts have increased about $80,000 as well in this time period. I traveled to 26 National Parks (some multiple times), visited every member of my family across the West during a pandemic, lost 60 pounds, and generally just crushed it. I can’t give YNAB credit for the weight loss or the National Parks, but I can say it’s been the central tool in almost every decision I’ve made, kept me on course, allowed me to achieve so much more than I could have imagined in such a short time. Thanks, YNAB, you’ve earned your $84. Start your own free trial of YNAB, no credit card required. My Financial GoalsBefore my next birthday, I want to:

I follow a lot of FIRE stuff but I don’t think I actually want to quit and never work again because I like what I’m doing with my side business. I want to see it succeed. Do I want to work my business 40 hours a week? No—I want to travel, quit my day job, and have the ability to generate income to support my lifestyle. I don’t have goals to buy a house, I’ve been doing the RV thing for 15 months. I can see myself doing this for another three or four years. Maybe somewhere along the way I’ll meet someone who’s worth stopping for. Or, I’ll say OK cool, maybe not. And I’ll live overseas and travel Europe. Either way, it’ll work out. I would rate my current financial situation: 5/5 A Financial Counselor ReactsI’m Rachel, a writer and an Accredited Financial Counselor® here at YNAB. I had the pleasure of talking to The Wanderer for this YNAB Snapshot. First, I just cannot even put into words how impressive this turnaround has been. And in such a short amount of time! If I could just have an ounce of the wanderer’s grit…whew what could we even accomplish?! I really liked hearing the thought process behind The Wanderer’s financial decisions. She really thinks through all angles and makes the choice that’s best for her situation: take the cash inflow and the outstanding debt, for example. Advice from other financial gurus might be to go headfirst, or four-legged-graceful-creature intense to knock out that debt. BUT, she’s choosing to keep it and keep her options open. I really liked that, and I love that she’s making a bet on herself. The interest rates on the truck and RV are reasonable (sub 5%), and it’s also not unlike having a mortgage payment, as her RV/truck setup is her primary residence. Sure, it probably won’t appreciate like a house (though who knows…car prices are crazy this year), but thinking of the expense as an accepted sunk cost: I can get behind that. For The Wanderer, I really had to dig to find something, I really like her budget setup, I like her approach to saving and maxing out those retirement accounts. My two thoughts: What matters more: earning an extra $200-$300 this year, or having a simplified bank account setup? The Wanderer: “Yeah, I’ve definitely thought that through. The rates are so piddly, I don’t know that it’s worth it to add another bank account. If interest rates improved? Eh, maybe. Now? Probably not.†2. Is there any further way we could simplify your financial life? You’ve got three credit cards you just paid off (HUZZAH!!). What’s your plan there for keeping them open or closing them? If you get to a point where you don’t really need to take out a big loan in the next few years, consider closing two of the three and just leaving one open. By the way, what is your credit score? The Wanderer: “820.†Ok, then! It doesn’t get much better. Absolutely nothing to worry about there. Credit scores take a bit of a hit when you close down a line (or three) of credit, but honestly—the more you use YNAB, the more you realize credit scores aren’t as important as you might’ve believed. Buying a house or a business loan would be the exception: you want to keep that perfect score for a large loan like that. Each fraction of a point adds up there! The Wanderer: “Yeah, the Alaska card annoys me with its yearly fee. But having them all is doing great things for my credit score, and I make occasional purchases on them. More likely, I’ll keep them open.†And with that, this money snapshot reaches its end. Who knows what The Wanderer will do next—rafting down the Grand Canyon? Driving Porsches on a test track? We’re not sure—but her Wish List is full so it’s just a matter of time before those things become a reality too. Want to gain total control of your money? Get started with your own budget and make your full-time RV living dreams come true! The post See My Budget: I’m Living Full-Time in an RV appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/see-my-budget-im-living-full-time-in-rv_3.html October 03, 2021 at 12:42AM

See My Budget: I’m Living Full-Time in an RV

Want to dive into full-time RV living but wondering the details of the financials? See how a full-time RVer traveling the country is making the most of her monthly inflows without sacrificing her financial goals. About

Income: $89,000+/year (variable depending on business)

Savings: $53,000

Debt: $62,500

I debated paying off my loans when the house payment came in, but after talking to a wise friend, they said it might be nice to keep my options open with that cash. So, I see it as FU money—it’s a year’s worth of expenses. My side hustle is doing well and this might allow me to go full time. Average Monthly Inflow: $5,000+/month

My BudgetI’ve been a YNABer since March 23, 2020: the day I moved out. I’ve got a lot of categories, but I like having them all split out so I can see how costs are broken down. Budget

Expenses Specific to Full-Time RV LivingThere are a bunch of things in my budget specific to full-time RV living:

My StoryIn late March 2020, when the world was shutting down, I finally called it quits on my marriage. Best decision I will make in my life. There were a lot of issues in our relationship, but the worst to me was his total disconnect and denial about spending within our limits. In five years, we spent $115k more than we brought in—burning through my $75k in pre-marriage savings and accruing $40k in credit card debts. I moved out with less than $400 in the bank, almost $20k on credit cards (we split the $40k credit card debt equally), and assumed the responsibility for the loan on our one-year-old RV. He kept the house, the car, and the majority of our stuff. I just wanted out. My plan was to move into the RV and travel the US seeing National Parks. In addition to the debt I already had, I had to buy $37k worth of a big diesel truck to make those dreams happen. I also needed to build an emergency fund. I work for an educational non-profit making $66k/year and I get $1,100 a month in Veterans Disability Pay. That’s less than $4,800 a month in take-home pay. I wasn’t even making it paycheck to paycheck. RV life isn’t cheap if you are on the move, so I cut my expenses down to the bare bones to make ends meet and started hustling hard:

With all that hustling and scrimping:

Between my hustling and the house settlement, it’s all about $87,000 total between paying off debt and cash saved since the divorce. That’s not counting my retirement funds, where I unintentionally managed to max out my 403b last year. Combined with a truly bumper year on the stock market for me, those accounts have increased about $80,000 as well in this time period. I traveled to 26 National Parks (some multiple times), visited every member of my family across the West during a pandemic, lost 60 pounds, and generally just crushed it. I can’t give YNAB credit for the weight loss or the National Parks, but I can say it’s been the central tool in almost every decision I’ve made, kept me on course, allowed me to achieve so much more than I could have imagined in such a short time. Thanks, YNAB, you’ve earned your $84. Start your own free trial of YNAB, no credit card required. My Financial GoalsBefore my next birthday, I want to:

I follow a lot of FIRE stuff but I don’t think I actually want to quit and never work again because I like what I’m doing with my side business. I want to see it succeed. Do I want to work my business 40 hours a week? No—I want to travel, quit my day job, and have the ability to generate income to support my lifestyle. I don’t have goals to buy a house, I’ve been doing the RV thing for 15 months. I can see myself doing this for another three or four years. Maybe somewhere along the way I’ll meet someone who’s worth stopping for. Or, I’ll say OK cool, maybe not. And I’ll live overseas and travel Europe. Either way, it’ll work out. I would rate my current financial situation: 5/5 A Financial Counselor ReactsI’m Rachel, a writer and an Accredited Financial Counselor® here at YNAB. I had the pleasure of talking to The Wanderer for this YNAB Snapshot. First, I just cannot even put into words how impressive this turnaround has been. And in such a short amount of time! If I could just have an ounce of the wanderer’s grit…whew what could we even accomplish?! I really liked hearing the thought process behind The Wanderer’s financial decisions. She really thinks through all angles and makes the choice that’s best for her situation: take the cash inflow and the outstanding debt, for example. Advice from other financial gurus might be to go headfirst, or four-legged-graceful-creature intense to knock out that debt. BUT, she’s choosing to keep it and keep her options open. I really liked that, and I love that she’s making a bet on herself. The interest rates on the truck and RV are reasonable (sub 5%), and it’s also not unlike having a mortgage payment, as her RV/truck setup is her primary residence. Sure, it probably won’t appreciate like a house (though who knows…car prices are crazy this year), but thinking of the expense as an accepted sunk cost: I can get behind that. For The Wanderer, I really had to dig to find something, I really like her budget setup, I like her approach to saving and maxing out those retirement accounts. My two thoughts: What matters more: earning an extra $200-$300 this year, or having a simplified bank account setup? The Wanderer: “Yeah, I’ve definitely thought that through. The rates are so piddly, I don’t know that it’s worth it to add another bank account. If interest rates improved? Eh, maybe. Now? Probably not.†2. Is there any further way we could simplify your financial life? You’ve got three credit cards you just paid off (HUZZAH!!). What’s your plan there for keeping them open or closing them? If you get to a point where you don’t really need to take out a big loan in the next few years, consider closing two of the three and just leaving one open. By the way, what is your credit score? The Wanderer: “820.†Ok, then! It doesn’t get much better. Absolutely nothing to worry about there. Credit scores take a bit of a hit when you close down a line (or three) of credit, but honestly—the more you use YNAB, the more you realize credit scores aren’t as important as you might’ve believed. Buying a house or a business loan would be the exception: you want to keep that perfect score for a large loan like that. Each fraction of a point adds up there! The Wanderer: “Yeah, the Alaska card annoys me with its yearly fee. But having them all is doing great things for my credit score, and I make occasional purchases on them. More likely, I’ll keep them open.†And with that, this money snapshot reaches its end. Who knows what The Wanderer will do next—rafting down the Grand Canyon? Driving Porsches on a test track? We’re not sure—but her Wish List is full so it’s just a matter of time before those things become a reality too. Want to gain total control of your money? Get started with your own budget and make your full-time RV living dreams come true! The post See My Budget: I’m Living Full-Time in an RV appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/10/see-my-budget-im-living-full-time-in-rv.html October 01, 2021 at 04:43AM

Public School Versus Private School: Why More Public Schools Will Rank Higher Over Time

As a public school graduate and parent, the debate between public school versus private school is fascinating. I think for the vast majority of people, going to public school and handing your kid a $1 million check upon graduation is the way to go. Posts mentioned: https://www.financialsamurai.com/why-public-schools-will-rank-higher-than-private-schools/ https://www.financialsamurai.com/the-wide-implications-of-the-college-admissions-bribery-scandal/ https://www.financialsamurai.com/accept-1000000-to-attend-public-school-over-private-school/

via Blogger http://shandradotson.blogspot.com/2021/09/public-school-versus-private-school-why.html September 25, 2021 at 10:42AM

Small Business Budget: See a Real Example

Working on your small business budget but not sure where to start? Sometimes it’s helpful just to see a real-life example to help you create your budget. This post will show you:

Without further ado, see how Izzy—a designer and small business owner—runs her company’s finances using a YNAB budget for a calm and stress-free financial setup. About

About the Business

Typical Business Revenue and Profit

The pandemic cut down on wholesale orders, paused in-person craft shows and events, and delayed many weddings so my business slowed down a lot last year. Cash on Hand

The cash I have on hand varies a lot throughout the year. Jewelry, like many product-based handmade businesses, is a very seasonal business. The holidays make up a large part of my annual revenue. Debt: $0

While I’m very thankful they’ve both been forgiven, applying was very stressful—the guidance kept changing! With the money from the assistance, I invested in a website redesign from a small design firm. Even before the pandemic I was trying to do fewer in-person markets, so this was a way of investing in building towards more online sales and supporting another small, creative business whose work I’ve admired. Average Monthly Inflow: $3K-$20KBecause fine jewelry is so seasonal, my inflows vary quite a bit. In my busiest months (November/December), I could bring in $20,000—while in one of my slower months (like March), it might only be $3,000. My Small Business BudgetBudget

About My BudgetMy small business budget is set up in YNAB and it’s worked really well to measure my financial health and help with short and long-term planning. I keep my owner’s draw category at the top of my budget to keep the number in front of me. I found early on in my business I was so excited about the idea of “business expenses†that it was easy to fritter money away. It’s all a tradeoff—every time I buy something, it could mean you can’t pay yourself as much, and I’m reminded of that tradeoff every time I open my budget. I file taxes as a sole proprietor (Schedule C for taxes). To make it easier for tax purposes, I set up my budget to include the corresponding line number of the Schedule C form. Accounting software like Quickbooks and Xero do these things behind the scenes, but I do it actively in YNAB. There’s an accounting firm called Sunlight Tax that specializes in accounting for creative small businesses that also provides a lot of education—I took a workshop with them and learned so much about better organizing my bookkeeping and how to create a business budget. The owner, Hannah Cole, was actually on the YNAB podcast talking about how artists and creatives can simplify their taxes. How I Manage Money with My Small BusinessTo manage money in my business, I use:

I used Quickbooks Online in previous years as my small business budget—mostly because I thought it was what “real†businesses used and because it was what the accountant I was working with at the time recommended. But I found YNAB was even more helpful in decision making and planning. In YNAB I can see my runway based on the money I had in my accounts—literally the period of time I have until the money in my accounts will run out and what it will cover. Seeing my income and expenses in this light empowered me to invest in the website redesign project because I could see exactly what would happen in my budget if I moved money to a “website†category. I like that YNAB lets you take care of what you need to for tax compliance but also serves as a decision-making tool when you’re budgeting for your business. Learn how to set up a business budget in YNAB. A few times a week, I’ll pop into my budget to import and categorize transactions. Friday is my big day to do money things:

I set up Square, Shopify, and Stripe to deposit once a week on Thursdays, so the money is there on Friday to allocate. With my business budget, I’m always a month ahead with expenses: when money comes in, I budget out a month before I fill up my owner’s draw category and start filling in other more “optional†categories. For example, when I flip into October, I’ll go into November’s set expenses and fill those up. For taxes, I’ve worked with an accountant before but this past year I did my own taxes because I’m very interested in them (thanks to Sunlight Tax!). I think generally it does make sense to work with an accountant and I really liked the one I worked with previously. Every quarter (September, January, April, June), I sit down and figure out my profit. Based on that number, I submit my estimated taxes. When it comes to April’s annual taxes, the self-employment tax I owe has already been submitted and I’m usually pretty close to the right amount. How I Got into Running My Own Small BusinessI was an English major and I’ve always been creative. I never set out to start my own jewelry line, but after working for a number of other design studios I decided to take the leap. As a creative, I think I’d always been told I wouldn’t like the numbers side of running a business. I’d absorbed the narrative that creative people don’t like money. That’s not true and not helpful. I went through a community-based entrepreneurship training during the first year of running my business that went over basic business financial topics like running a breakeven or cash flow analysis. It turned out I actually love the numbers side of the business—it’s so interesting. The business is now five years old, and the creativity never stops when I leave my studio. To me running a business feels like a holistic creative practice—figuring out logistics like shipping and packaging, determining how to learn the new skills I need, structuring my budget and constantly re-evaluating how to best use the resources I have available—it’s all deeply creative. My Financial GoalsWhen it comes to business performance, I want to shift to more online-centered sales so I don’t have to travel as much as I had before the pandemic. I’d like to break $100,000 in revenue and make the business more profitable as time goes on too. Early on, I was spending money on accumulating equipment and tools, so much of the money I was making was going straight back into growing the business. Personally, we’re saving for a down payment and I’d love to build a tiny house or freestanding studio in the backyard for my business. In the big picture, running my own business gets myself and my partner closer to our goal of financial independence, and having control over our time. I would rate my current business financial situation as a 3.5/5. I’m working towards building more revenue and streamlining the business to make it more profitable but I also feel truly proud of how far the business has come. But I would rate my current peace around finances: 5/5. I feel clarity around what I want to do with my business resources and after having been in business for a few years not too many variable costs truly surprise me anymore. You’ve been perusing small business budgeting templates, are you ready to turn one into the real thing? Learn more about using YNAB to manage your small business budget. The post Small Business Budget: See a Real Example appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/09/small-business-budget-see-real-example.html September 22, 2021 at 04:42AM

We’re Hiring a Part-Time Seasonal Support Rep!

Do you enjoy customer support? Want to kick off 2022 with some extra money in the bank? Are you excited about helping YNAB users start the New Year with their budgeting on track? If you answered yes to all of these questions—read on! We are looking for tech-savvy, friendly, Seasonal Customer Support Specialists to help this holiday season. This is a temporary, part-time (25-29 hours per week), remote position beginning in mid-November 2021 and going through mid-February 2022. If you’re a YNAB user already (or willing to learn it!) and are known for being helpful, patient, and awesome, we want to hear from you! A Bit About UsWe build “You Need a Budget,” the best budgeting software and educational resources around. (But people in the know call us YNAB, which is pronounced “why-nab”). For more than a decade, people have been using YNAB and then telling their friends what a difference it has made in their lives. Google us, or read some of our reviews on the app store, and you’ll see what we mean. We love building something that has a huge positive impact on people’s lives. We love our YNAB customers, and we want to make sure they love their support experience. Our support specialists look forward to every email, because it’s an opportunity to help another person gain control of their money and become a better budgeter. We have one overarching requirement when it comes to joining our team—even temporarily: our Core Values have to really click with you. If you’re nodding emphatically while reading it, you’ll probably fit right in! Requirements:

More About Our Ideal Seasonal Support Rep…January is our busiest time of the year! We receive thousands of messages from old and new YNABers alike who want to start off the year on the right foot. We want you to join our dedicated support team to help us answer each of these messages in a friendly and timely manner. You will be the face of YNAB. We’ll train you to answer the most common questions our users have so you’ll be able to make a difference from your very first shift. You won’t mind answering the same question multiple times in the same shift, because it’s a different customer each time—another chance to make someone’s day. You’re also able to change gears relatively quickly. You may answer multiple credit card questions in a row, then effortlessly switch to a direct import issue when you come across it. You manage to exceed expectations even when you deliver a different answer than the customer was hoping for. You know that speed of response is extremely important, but you can walk that fine line between speed and accuracy. You are a master of being direct and friendly within the same sentence. You’re a team player. You know that your performance impacts the team as a whole, and are constantly striving to make yourself, and thus the team, better. You love taking that one little extra step beyond what’s expected. You’re creative in that way. Who You’d Be Working With:Natalie & Renae lead our support onboarding team at YNAB, which means they have the incredible privilege of walking you through all the ins and outs of YNAB support. Natalie does a great job of managing the onboarding team and Renae is the senior support specialist who’s always willing to lend a hand. They’re available to answer questions, support you in your 1:1 meetings, and give plenty of virtual high-fives. Your team of fellow seasonal support reps will likely be some of the best people you’ve ever worked with. You may be spread over the globe, but you’ll come together in your Slack (our internal communication platform) channels for a quick hello before hopping into the queue. A Day in the Life:You’re typically scheduled for a five hour shift, but things are busy in the queue this week and you have some flexibility in your schedule, so you offered to work six hours today. That extra hour means even more users you get to delight with your responses. You start your shift by checking for any recent updates and announcements. Once caught up there, you close Slack to minimize distractions as you head into the queue. Your first stop is your follow-ups. You had yesterday off, so your teammates took care of most of them, but there are a few that came in earlier this morning—including some from users letting you know your last responses solved their issues perfectly, so your day is off to a great start! Then, you head to the back of the queue and pick up a couple of the oldest conversations. You’re often surprised by the complexity of the questions you see, but you’re excited for the challenge each one brings. And you know you can skip the ones beyond your level, and plan for some time out of the queue to fill in those knowledge gaps. Today you have your one-to-one meeting with your manager, so you pop in your headphones and hop on a video call to talk about your metrics, goals, and some tricky conversations you want a second opinion on. Before you know it your work day is over, so you say goodbye to your team in Slack, change your Slack status, and quickly scan your task list and calendar for tomorrow. Satisfied with the day’s work, you close your laptop and move on with the rest of your day. You’re Who We’re Looking for If:

Bonus Points:

Pay for this seasonal position will be $17 USD per hour. YNAB is an equal opportunity employer. We believe diversity of backgrounds, beliefs, abilities, and experiences to be critical to our success and are passionate about creating a welcoming, supportive, and collaborative environment for all employees. All are encouraged to apply as we continue to grow a smart, hard-working, and diverse team who love working together to build something that matters. How to ApplyPlease note that while YNAB is fully remote, because this particular role is a short-term, temporary position, you must either live outside the U.S. or live in one of the following states: Arizona, Arkansas, California, Connecticut, Colorado, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Kentucky, Maine, Maryland, Massachusetts, Michigan, Minnesota, Missouri, Montana, Nevada, New Hampshire, New Jersey, New York, North Carolina, Ohio, Oklahoma, Oregon, Pennsylvania, Tennessee, Texas, Utah, Vermont, Virginia, Washington, Wisconsin.

We can’t wait to hear from you! P.S. We’ll send you a confirmation email once you apply. Please add that email to your safe sender list, to ensure that future emails come through. (If you don’t receive it, please check your promotions inbox, junk folder, or any filters you may have set up.) The post We’re Hiring a Part-Time Seasonal Support Rep! appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/09/were-hiring-part-time-seasonal-support.html September 17, 2021 at 07:42AM

The Best Time To Go To Work Is During A Pandemic

Is the grass greener on the other side? Maybe! But it sure seems like work is awesome for knowledge workers during the pandemic. I discuss this topic with my wife. We'll talk about public school rankings later! Posts mentioned: How To Convince Your Spouse To Work Longer So You Can Retire Earlier via Blogger http://shandradotson.blogspot.com/2021/09/the-best-time-to-go-to-work-is-during.html September 16, 2021 at 01:42AM

Budgeting with ADHD

Sometimes it seems as though adulthood is one very long obstacle course. It’s all either smooth sailing and easy wins or lessons that require special training and repeated attempts to overcome. That analogy is particularly true for people with adult ADHD/ADD. You may know exactly what needs to be done to get through each day, but the actions required to complete the tasks might not come naturally without implementing some life hacks to help make it happen. Benefits of Budgeting with ADHDCreating a budget is more than just sitting down with your expenses and making a spreadsheet; it involves setting up a system, changing your mindset, and incorporating some accountability in order to make it all stick. Sounds boring, right? Yeah, oddly enough, budgeting apps don’t get near the same hype as video games or the newest HBO original series. But, let me ask you this…did Game of Thrones help you avoid overdraft fees? Did Grand Theft Auto help you break the paycheck to paycheck cycle? (Legally?) Think of setting up your budget like training to complete an obstacle course. Sure, the push ups and sprinting and falling off of ledges isn’t a ton of fun, but winning American Ninja Warrior? That would be super fun. You’re going to be the Intergalactic Budgeting Ninja Warrior. Or something. For adults with ADHD/ADD, budgeting is more than money management, it’s a system put into place to give your brain a break from remembering (and/or avoiding) the jumble of due dates, bills, balances, and the informal, and often inaccurate, mental math necessary to justify (or regret) yet another impulse purchase. Think of your budget like a little butler who follows you around carrying the load that the uncertainty of disorganized finances can bring. That guy is your friend! Is it annoying when he tells you that you shouldn’t get takeout tonight? Absolutely, but you’ll thank him when you don’t have to call your landlord to explain that you spent your rent money on tacos. Again. Mmmm, tacos. The Best Budgeting App for ADHDThe best budgeting app is whichever one that you’ll actually use, but the YNAB app and proven method has some benefits that may be particularly helpful in serving as a detour for the roadblocks that are most likely to pop up as the result of ADHD/ADD symptoms. The Four Rules:If you find yourself feeling easily disorganized, YNAB’s Four Rules simplify the philosophy and methodology of budgeting in a way that changes how you think about money. Incorporating YNAB’s Four Rules into your daily life creates a set of guidelines about how to prioritize your spending, to expect the unexpected, to allow yourself some flexibility (and forgiveness), and to stop living paycheck to paycheck. YNAB’s Four Rules of Budgeting Are:

ADHD-Friendly Budgeting FeaturesYNAB was designed to integrate budgeting into your daily life without becoming a tedious or overwhelming chore. Here are a few of the features that will help keep you on track: Direct Import: If you choose to link your bank account to your budget, all of your transactions will import automatically. No more losing receipts, forgetting how much you spent, or trying to do on-the-spot subtraction under pressure to see if you can afford something. You simply look at your budget, and it will tell you if you have money available to spend in the category you’re considering. Accessibility: Let’s be honest with ourselves—after a long day of work, chores, and life in general, sometimes it can be hard to talk yourself into firing up the laptop to engage in a relaxing budgeting session. YNAB’s mobile app makes it easy to check your available funds at a glance and on the go, and makes it possible to enter, approve, or match transactions when you’re looking for a midday distraction. Conversely, with the web app, you can take a budgeting break from your work day on your laptop. Your budget is basically everywhere you go.

Customizable categories: Budgeting isn’t one-size-fits-all and your method for organizing your expenses doesn’t need to be either. Although YNAB starts you off with a basic template that makes sense to us, maybe you think about your budget categories differently. Regroup, reorder, rename, add emojis for a quick visual reminder, create an entire category group dedicated to your favorite snack items in order of preference…do whatever you want. It’s your budget. Make it as fun as budgeting can be. Flexibility: Some budgeting apps and advisors are awfully judgy about how you spend your money. YNAB knows that a lot of people are going to skip budgeting altogether if it introduces yet another source of guilt, shame, or feelings of inadequacy in your daily life. Remember Rule Three? (Psst…it’s to Roll With the Punches.) We’re not here to tell you how to spend your money, we’re here to help you manage it. Budget for what you want, move money around, forgive yourself if you fall off the financial wagon, plant a wish farm, and be kind to yourself while you learn.

Auto-Assign: Need some help prioritizing your expenses? Or not into spending too much making decisions about your dollars? Auto-Assign will offer suggestions based on due dates and prior spending habits with the push of a button.

Credit Card Management: When you add your credit cards to YNAB, your budget encourages you to categorize your credit card spending and then shuffles money from its “Available” spot directly to your credit card payment category. Bought toilet paper at Costco on your Visa card? Categorize it as a household good, specify that you used your Visa, and your little YNAB budget butler says, “Oh, hey, we’re not going into debt for toilet paper, so let me take that amount out of your ‘household goods available funds’ envelope and stash it in your ‘Visa payment available funds’ envelope. No more feeling bad when the credit card statement shows up and there’s not enough money to cover it. Spending and savings targets: There are bills that are due at the same time every month for about the same amount, expenses that pop up just irregularly enough to make them forgettable, and savings goals that we hope to reach eventually. It’s a lot to keep track of. Setting targets in your budget can help you remember how much to set aside, how much you’ve already assigned to that category, and provide a colorful visual reminder of your progress.

Scheduled Transactions: Setting up automatic payments for your bills is a real lifesaver if you’re not good with due dates, but can be a frightening prospect when you’re not confident that the money will actually be there. Go ahead and do it, set a budget target, and add a scheduled transaction for the future. You won’t have to think about it again until YNAB asks you to match it to your bank transaction, and by then it’s a done deal. No more late payments. Built-In Support and AccountabilityBudgeting can be a challenge for anyone, but budgeting with ADHD presents a special set of obstacles. Creating a budget in YNAB gives you one source of truth—you can check your budget instead of your bank account so that you can easily visualize your finances and see if you really have money to spend or not. The act of giving your dollars jobs each time you get new money, approving transactions as they pop up, and reconciling your budget helps keep you connected and engaged to your current financial state without overwhelming you with a ton of random tasks or irrelevant information. Last, but definitely not least, YNAB changes the way you think about money. You can learn about personal finance, about budgeting, and about YNAB in whatever way works best for you. Enjoy podcasts? Perfect! Are you a video viewer? We’ve got those! Do you remember best by reading blog posts or help docs? Lots of options there. Need weekly tips and tricks delivered to your inbox? We’re on it. Looking for a community to bounce ideas off of, Q&A sessions, or one-on-one support? We’ve got you! Ready to get started? Sign up for a free 34-day trial today—and don’t worry, there’s no credit card (or commitment) required. The post Budgeting with ADHD appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/09/budgeting-with-adhd.html September 15, 2021 at 04:42AM

How to Start YNAB in the Middle of the Month

There’s this weird psychological trick some of us play on ourselves where we decide that the best time to start a new diet, routine, or budget is on a Monday. Or on the first of the month. Or on the first of the year. Pretty crazy how that doesn’t apply to starting a new book, video game, or Netflix series, huh? Yeah, that tactic is actually just a cleverly garnished cocktail of procrastination, anxiety, and dread. The best time to start a budget is now—yes, even if it’s a Wednesday, or the 15th of the month, or the 11th month of the year. And here you are! Rock on! And studies show that you’re actually MORE likely to succeed with a new habit if you pick an arbitrary start day. Like today! Think of it this way: if you start now, you’ll already be familiar with your new habit by the first of the month. Ahead of the game, even. If it was a race, you’d be leaving those, “I’ll do it later,” people in the dust and who doesn’t love to win? Get Ready: What You’ll Need to BeginIn reality, starting a budget in YNAB in the middle of the month is not more difficult. Money touches our lives every day—it’s not like all of our bills are due on the first, or like there’s some two day pause between months where everything resets perfectly. Go gather up the following and meet us back here at the starting line:

Ready to go the distance? Get Set: Categories and TargetsThe next step is to create categories and targets for each of your expenses. Think of your categories as envelopes full of cash. You’ll take a blank envelope, write “mortgage” on it, put the amount due and the due date in the corner, and fill that envelope with the appropriate amount of money before that due date rolls around. But our way is much easier than shuffling paper money and digging around in envelopes to see how much you have. CategoriesList your expenses as categories, and feel free to come up with a snazzy name or to add a cute emoji. You might as well make it fun. You can also organize your categories by due date so that you can visualize and prioritize your month more easily. Just drag and drop on the web app, or hit the “edit” pencil and long press on the three lines to drag and drop on mobile. You can hide or delete categories if you get a little category-crazy. Just click on the category name on the web or on the minus sign in the edit screen on mobile to find those options. Your best bet is to keep your categories as simple as possible while you get started.

TargetsStep one of winning a race is knowing where the finish line is! Probably. I don’t know because I don’t run but I really think this would be a critical component.

Anyway, spending and savings targets are like the finish line for funding your categories each month. You can choose to set Weekly, Monthly, or By Date spending targets, depending on the type of expense:

You set targets by hitting the edit pencil on mobile, or by clicking within the category on the web. Go! Add Accounts and Assign Your MoneyNow you’re really off to the races. First, add your banking and credit card accounts to your budget. Linked AccountsYou can choose to link your account to your budget and your balance and transactions will automatically update. (Yes, you can trust YNAB.) Unlinked AccountsIf you’d like to be a little more hands-on with your money management, you can enter your transactions and input your balances manually. And actually, our teachers heartily recommend new YNABers enter their transactions yourself for the first week as you’re getting started. Credit CardsDon’t sleep on adding your credit cards to your budget, just make sure that you select Credit Card as the account type, because it changes the way you manage any existing debt.

Want to learn more about using credit cards in YNAB? It’s a popular request. Head on over to our blog post about YNAB and credit cards once you’re done setting up here. Savings AccountsIt may be tempting to skip adding your savings accounts to your budget. It makes a lot of people nervous to see the money they’re trying not to spend show up in the “Ready to Assign” balance. The good news is that you’re still not going to spend it. You’re going to assign it to the specific category that you’re saving for—this protects that money, keeps it separate when you view your budget, and creates some accountability around meeting your savings goals. Are you really going to borrow from your house downpayment fund for tacos for the second night this week? You’ll think twice about it when you have to move that money from one category to another.

Set up your savings account the same way you did for checking, just categorize it as a savings account when YNAB asks. (If you didn’t create savings categories upon your initial category set up, go do that now.) Assigning Money Mid-MonthThis is where the magic happens. Lace up your running shoes, my friends. (You don’t really have to wear shoes for any of this.) The key ingredient to the YNAB method is…well, all of them. There are Four Rules, and they’re all important. However, Give Every Dollar a Job is the muscle behind your momentum. Everything we’ve done so far has been warm up for this. Remember when you made your categories? Set your targets? Added your accounts? Now we’re ready to put each dollar to work. See your Ready to Assign total at the top? That’s how much money you have to populate your budget with right now. Don’t worry about money you haven’t earned yet—those dollars will get their jobs when they actually show up to work. Go down your list of categories in order of due date and/or urgency and ask yourself, “What does my money need to do before I get paid again?” Distribute your dollars between categories accordingly. Continue doing this until you reach zero in your Ready to Assign box. This is called zero-based budgeting and it helps you create more intention around spending your money. Since it’s the middle of the month, you may need to check your bank statement to see which bills have already been paid so that you have a more accurate idea of which categories to fund first. Also, if you’re halfway through the month, you can (probably) cut your grocery and dining out categories in half.

Step-by-Step Summary to Budget SuccessSo, basically we have Four Rules and three steps. To stay on the path to financial freedom, remember the following: YNAB’s Four Rules

The Three Steps Each Payday

Budgeting works whether you start it on a Monday, a Wednesday, the first of the month, the fifteenth of the month, or midway through the 182nd day of the year. The real key to budgeting is simply starting…so get ready, set, and go Give Every Dollar a Job. Interested in more budgeting tips and tricks? Say no more. We’ll bring them straight to you in our Weekly Roundup. The post How to Start YNAB in the Middle of the Month appeared first on You Need A Budget. Via Finance http://www.rssmix.com/via Blogger http://shandradotson.blogspot.com/2021/09/how-to-start-ynab-in-middle-of-month.html September 13, 2021 at 05:42AM |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

RSS Feed

RSS Feed